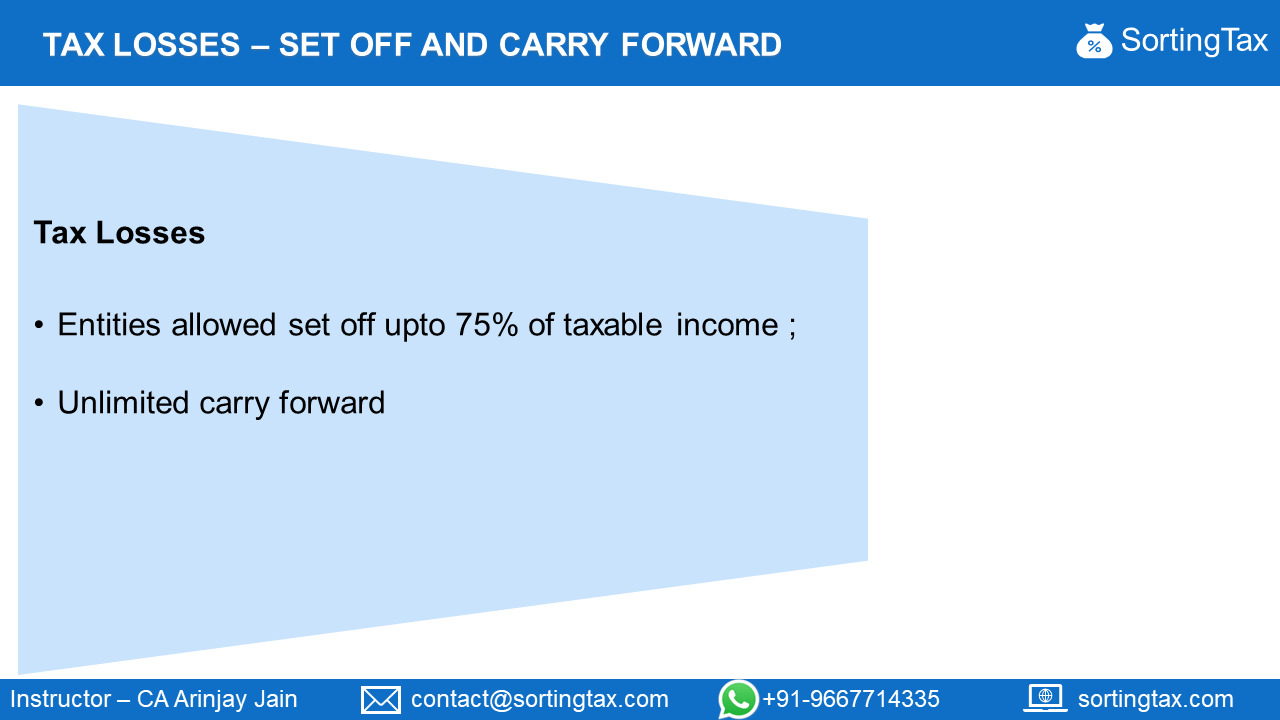

Tax Losses under UAE Corporate Tax – Set off and carry forward

Section 5 of the proposed UAE corporate tax outlines, the rules and regulations relating to the treatment of tax losses under the UAE corporate tax law.

By their very nature, businesses go through different cycles of profit and losses, wherein they earn profits in one year and losses in another year. This is more common at the initial stage of setting up of business, and may sometime due to market circumstances. If the business pays tax when they earn profits and loose cash when they suffer losses, it would be unfair to them on an overall basis.

Offsetting Tax Losses

Under the proposed corporate tax law, UAE businesses, who incur tax losses in business in certain years, can offset such loss of one Financial period against the taxable income, of future financial periods. However, the limitation is that the maximum loss which can be set off , in any period, shall be 75% of the taxable income of that future year.

Learn More about “Tax Losses under UAE Corporate Tax” – Subscribe UAE Corporate Tax Course

Carry forward of losses

Carry forward of tax loss, is a provision that allows a taxpayer to move tax loss incurred in a year, to future years , and offset against future profit to reduce the tax liability of future year.

Under the proposed law, a business is allowed to carry forward losses of one financial period, for unlimited time. However, in order to claim such benefit, 50% of the shareholders of the company should remain the same , from the beginning of the period when the business incurred loss , until the end of the period in which a loss is offset against taxable income.

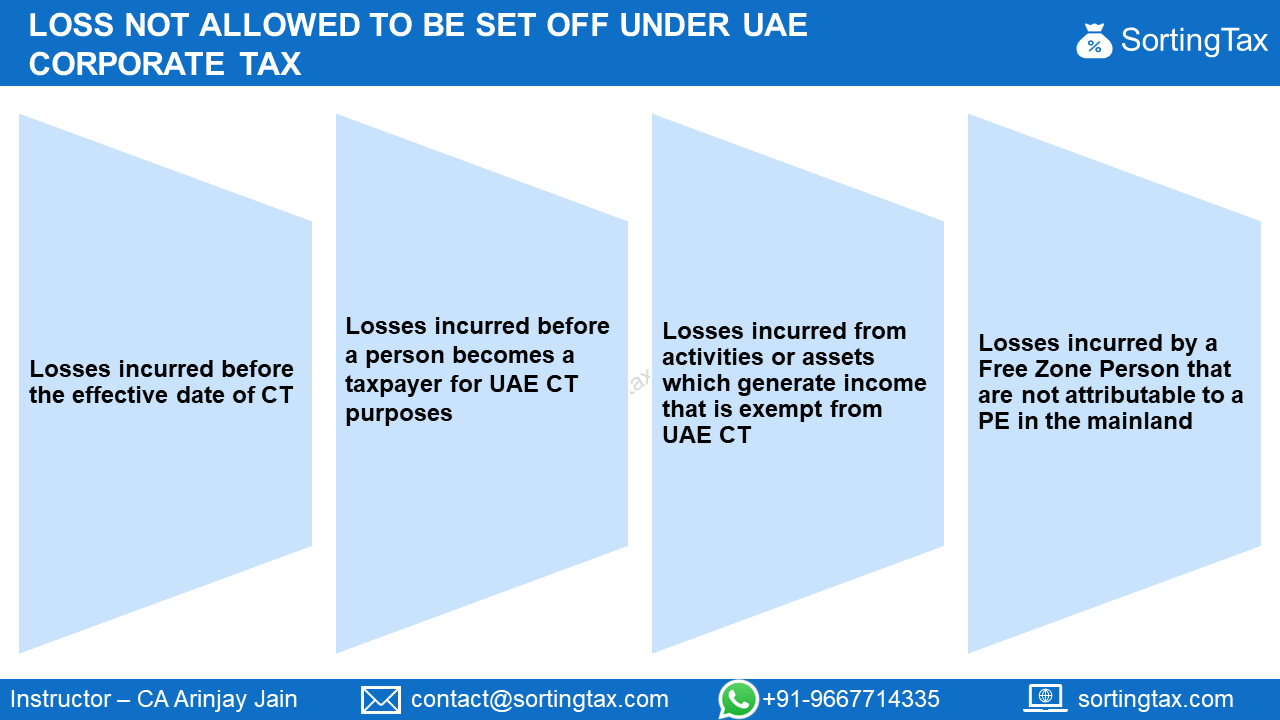

Loss not Allowed to be set off under UAE Corporate Tax

Limitations for claiming carry forward of tax loss

Under the proposed law, following losses cannot be offset or carried forward to a future period : –

- Losses incurred before the effective date of CT (in respect of that particular business) ;

- Losses incurred before a person becomes a taxpayer for UAE CT purposes

- Losses incurred from activities or assets which generate income that is exempt from UAE CT

- Losses incurred by a Free Zone Person that are not attributable to a PE in the mainland

Learn More about “Tax Losses under UAE Corporate Tax” – Subscribe UAE Corporate Tax Course

Case Study – Carry Forward of Losses

| NATURE OF INCOME | INCOME (AED) | AMOUNT (AED) |

| Taxable Income – 31.12.2025 | 15,00,000 | |

| Tax Loss B/f – 31.12.2024 | 8,00,000 | |

| Tax Loss B/f – 31.12.2023 | 8,00,000 | |

| TOTAL TAXABLE INCOME | ||

| LOSSES ADJUSTED | ||

| TAXABLE INCOME | ||

| TAX @ 9% | ||

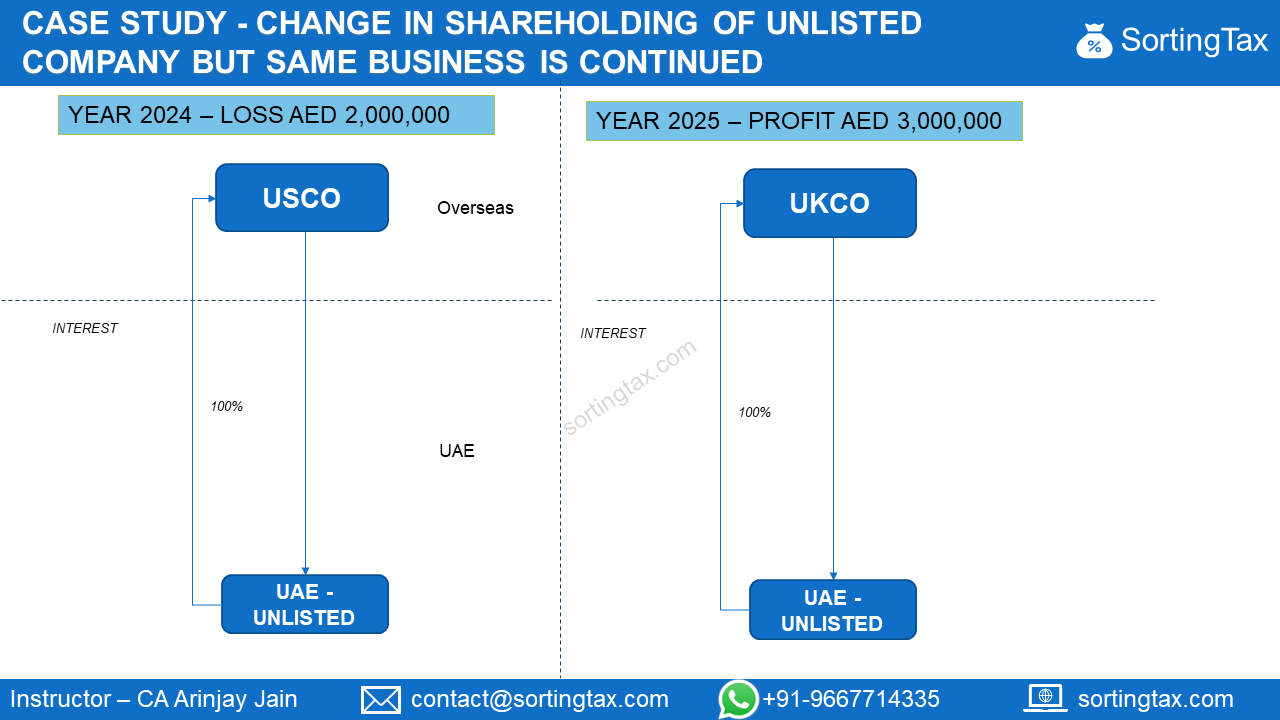

Case Study – Change in Shareholding of unlisted Company but same business is continued

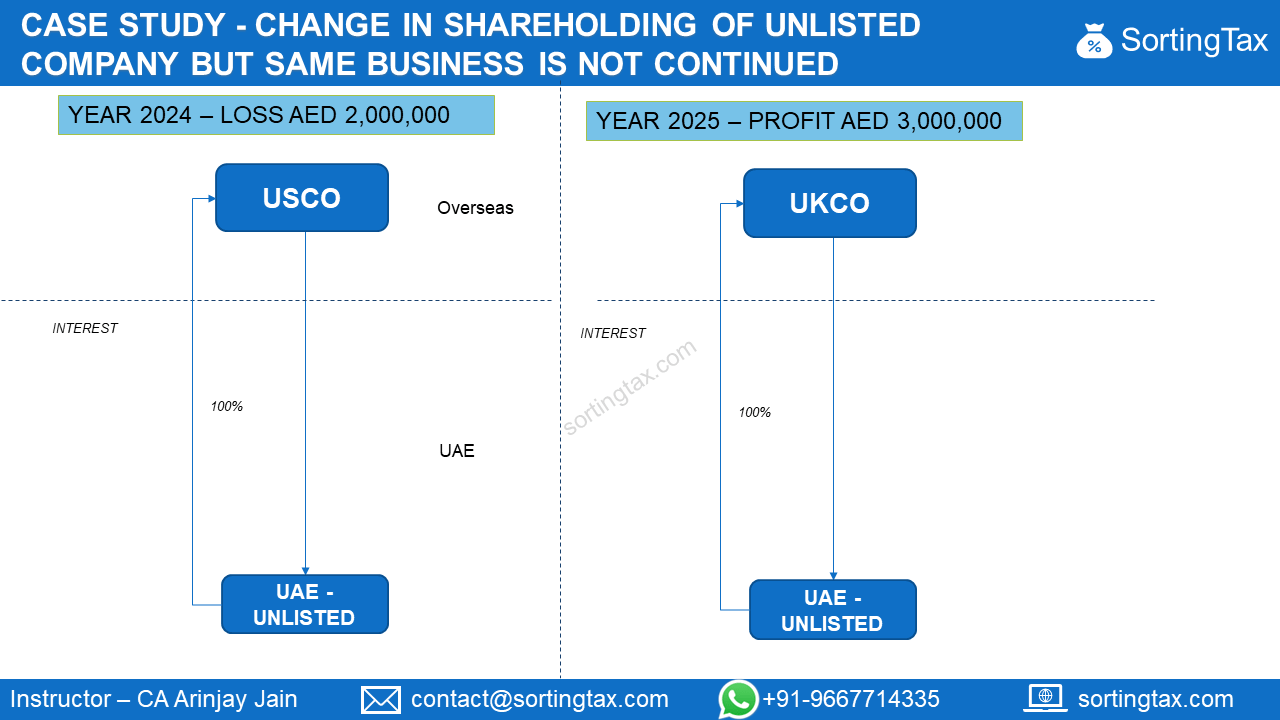

Case Study – Change in Shareholding of unlisted Company but same Business is not continued

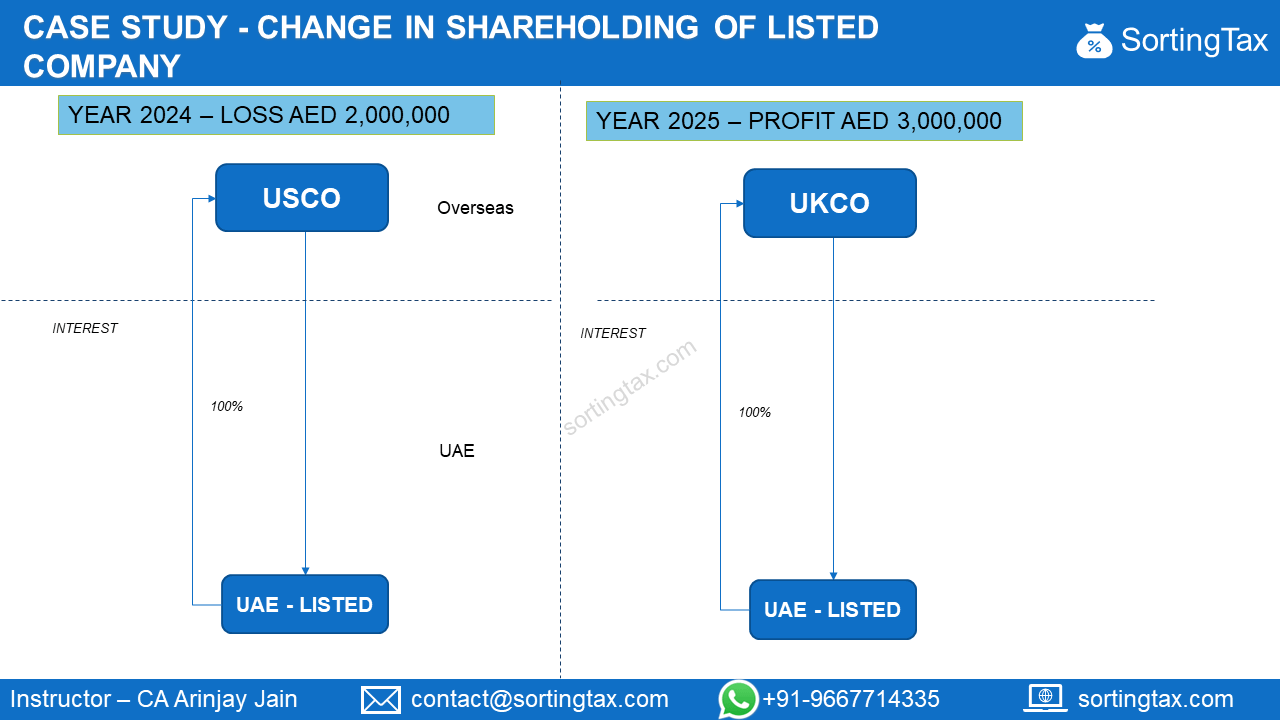

Case Study – Change Study – Change in Shareholding of Listed Company

Learn More about “Tax Losses under UAE Corporate Tax” – Subscribe UAE Corporate Tax Course