Article 2 – Taxes covered under Double Taxation Avoidance Agreement

This Article provides the details of taxes, which would be covered for the purpose of tax Treaty. Any tax which is not provided in Article 2 is outside the purview of the tax Treaty.

Article 2 defines the taxes, to which the Treaty shall apply. Generally, it applies to taxes on (a) Income and (b) Capital. Such taxes are imposed on behalf of a Contracting State or of its political subdivisions or local authorities and would be covered, irrespective of the manner in which they are levied, i.e, they could be levied directly or deducted as tax at source (TDS in Indian context).

Learn More about “Article 2 – Taxes covered under Double Taxation Avoidance Agreement” – Subscribe International Tax Course

Learn More about “Article 2 – Taxes covered under Double Taxation Avoidance Agreement” – Subscribe International Tax Course

One of the very basic question, which arises in the mind of a taxpayer evaluating Double Taxation Avoidance Agreement, is, Which taxes are covered under Double Taxation Avoidance Agreement ? Or in other words, can I claim the benefit of all taxes which may be payable in the source country, or only certain specific taxes are eligible for benefits?

Let us discuss these aspects in detail : –

WHY IS ARTICLE 2 RELEVANT?

- Only taxes covered under Article 2 are covered under Treaty.

- Ascertain if surcharge is to be applied in addition to Tax rates.

- Avoid need to renegotiate Treaty for changes on local levy ( India – SC + Education Cess )

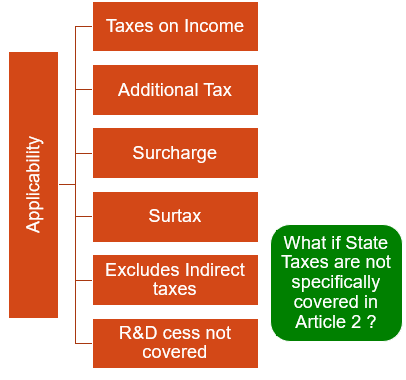

WHICH TAXES ARE COVERED UNDER ARTICLE 2 DOUBLE TAXATION AVOIDANCE AGREEMENT?

- Indirect taxes are not covered under Article 2.

- Non-Discrimination – Article 24 & Exchange of Information – Article 26 are applicable to all taxes.

- Research and development Cess not covered by Article 2 – ( Netherlands Treaty Protocol ).

ARTICLE 2 (1) – INDIA NETHERLANDS TREATY

This Convention shall apply to

taxes on income and on capital

imposed on behalf of

one of the States or

of its political subdivisions or

local authorities,

irrespective of the manner in which they are levied

Learn More about “Article 2 – Taxes covered under Double Taxation Avoidance Agreement” – Subscribe International Tax Course

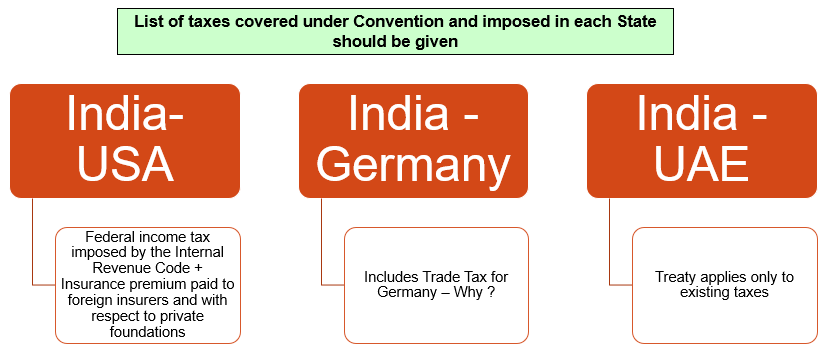

ARTICLE 2(1) – INDIA USA TREATY

The existing taxes to which this Convention shall apply are :

(a) In the United States, the Federal income taxes imposed by the Internal Revenue Code (but excluding the accumulated

earnings tax, the personal holding company tax, and social security taxes), and the exercise taxes imposed on insurance

premiums paid to foreign insurers and with respect to private foundations (hereinafter referred to as “United States Tax”);

provided, however, the Convention shall apply to the exercise taxes imposed on insurance premiums paid to foreign insurers only

to the extent that the risks covered by such premiums are not reinsured with a person not entitled to exemption from such taxes

under this or any other Convention which applies to these taxes ; and

ARTICLE 2(1) – INDIA USA TREATY

(a) in India : –

(i) the income-tax including any surcharge thereon, but excluding income-tax on undistributed income of companies, imposed under the Income-tax Act ; and

(ii) the surtax (hereinafter referred to as “Indian tax”).

Taxes referred to in (a) and (b) above shall not include any amount payable in respect of any default or omission

in relation to the above taxes or which represent a penalty imposed relating to those taxes

KEY FEATURES OF ARTICLE 2

WHICH TAXES ARE COVERED ?

ARTICLE 2 (2) – INDIA NETHERLANDS TREATY

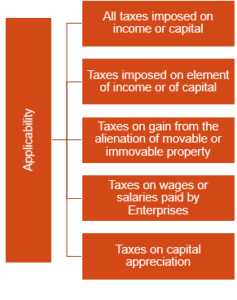

There shall be regarded as taxes on income and on capital

all taxes imposed on total income,

on total capital, or

on elements of income or of capital,

including taxes on gains from the alienation of movable or immovable property,

taxes on the total amounts of wages or salaries paid by enterprises,

as well as taxes on capital appreciation.

What shall be regarded as Taxes on income and on capital ?

Learn More about “Article 2 – Taxes covered under Double Taxation Avoidance Agreement” – Subscribe International Tax Course

Which Taxes are covered under Article 2 – Double Taxation Avoidance Agreement

KEY FEATURES

- Taxes on Income & Capital

• Income should be considered as per Section 2(24) of the IT Act, 1961

• Excludes (a) Property tax; and (b) Tax computed on a basis, other than income. - Whether “Tax” includes interest/ penalty ?

Interest and penalties are generally not considered as “Tax” under Indian Treaties - Capital Appreciation

UN Model considers taxes on revaluation of Assets . In India ? - Excluded taxes

Art 2(2) may exclude specific source State taxes.

ARTICLE 2(2) – INDIA USA TREATY

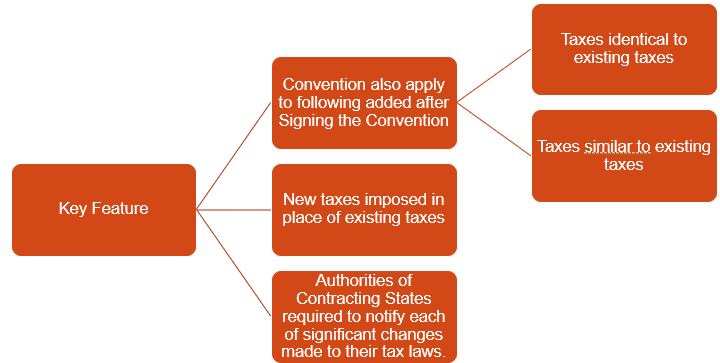

The Convention shall apply also to any identical or substantially similar taxes

which are imposed after the date of signature of the Convention

in addition to, or in place of, the existing taxes.

The competent authorities of the Contracting States shall notify each other

of any significant changes which have been made in their respective taxation laws and

of any official published material concerning the application of the Convention.

KEY FEATURE OF ARTICLE 2(2) OF INDIA USA TREATY

ARTICLE 2 (3) – GENERAL CLAUSE

The existing taxes to which the Convention shall apply are in particular :

(a) In the XYZ :

(b) In India :

Refer India USA DTAA referred above on Slide

ARTICLE 2(2) – INDIA UAE TREATY

1. ……

2. The existing taxes to which the Agreement shall apply are (added <<<>>>> ) : –

(a) In United Arab Emirates :

(i) income-tax ; (ii) corporation tax ; (iii) wealth-tax

(hereinafter referred to as “U.A.E. tax”) ;

(b) In India :

(i) the income-tax including any surcharge thereon ; (ii) the surtax ; and (iii) the wealth-tax

(hereinafter referred to as “Indian tax”).

ARTICLE 2(3) – INDIA GERMANY TREATY

The existing taxes to which this Agreement shall apply are in particular : –

(a) in the Federal Republic of Germany :

the Einkommensteuer (income-tax),

the Korperschaftsteuer (corporation-tax),

the Vermogensteuer (capital tax), and

the Gewerbesteuer (trade tax)

(hereinafter referred to as “German tax”);

(b) in the Republic of India,

the income-tax including any surcharge tax thereon (Einkommensteuer, einschl, darauf entfallender Zusatzsteuern), and the wealth-tax (Vermogensteuer) (hereinafter referred to as “Indian tax”).

KEY FEATURES OF ARTICLE 2(3)

Learn More about “Article 2 – Taxes covered under Double Taxation Avoidance Agreement” – Subscribe International Tax Course