International Transaction – Section 92B of Income Tax Act

Transfer Pricing provisions are applicable to determine the arm’s length price of ‘International transaction’ and ‘Specified domestic transactions” between Associated enterprises. Even though domestic transactions are covered in Transfer Pricing , generally Transfer Pricing provisions are mostly considered in the context of international transaction.

Thus, it is essential to understand the meaning of international transaction. If a transaction is not an ‘international transaction’, TP provision would not apply (except in case of specified domestic transaction”.

However, to understand the definition of “International Transaction”, it is first important to understand the definition of “Transaction”.

| Principle of International Taxation | Transfer Pricing |

| Transaction between | International Parties |

| Transfer Price | Price charged between two Associated Enterprises |

| Governing Provision |

|

| Conditions for an “International Transaction” |

|

International Transaction – Section 92B of Income Tax Act

Transfer Pricing provisions are applicable to determine the arm’s length price of ‘International transaction’ and ‘Specified domestic transactions” between Associated enterprises. Even though domestic transactions are covered in Transfer Pricing , generally Transfer Pricing provisions are mostly considered in the context of international transaction.

Thus, it is essential to understand the meaning of international transaction. If a transaction is not an ‘international transaction’, TP provision would not apply (except in case of specified domestic transaction”.

However, to understand the definition of “International Transaction”, it is first important to understand the definition of “Transaction”.

Definition of Transaction [Section 92F & Rule 10A(D)]

Sections 92F provides an inclusive definition of transaction. If a particular transaction is not covered within this definition, it may still amount to be a transaction for TP purpose. It defines as Transaction as under : –

“Transaction” includes an arrangement, understanding or action in concert,

a) whether or not such arrangement, understanding or action is formal or in writing ; or

b) whether or not such arrangement, understanding or action is intended to be enforceable by legal proceeding.

For computation of arm’s length price under Rule 10A of the Income Tax Rules, 1962 (“IT Rules”), Rule 10A(d) defines a “Transaction” as including number of closely linked transactions .

Readers Note : –

Section 92F provides an inclusive definition of the term “transaction”, i.e., it can include other transactions which are not specifically covered under the above definition. Based on the plain reading of this section, it is evident that, even if there is no formal written agreement, or any intention of the parties to legally enforce a transaction, it could still be a transaction for Transfer Pricing purposes.

Examples on meaning of transaction

Example 1: –

ICO Private Ltd. has a show room of home furnishings in New Delhi. Due to high demand of furniture during Diwali, ICO places an order for certain furniture and furnishings with FCO, the overseas parent of ICO. FCO agrees to supply the furniture to ICO on credit basis and agrees to formalize the arrangement after Diwali.

Would the transaction of sale of furnishing amount to a transaction ?

Solution : –

To constitute a transaction, it is not mandatory to have a formal written agreement. Transaction” includes an arrangement, understanding or action in concert, whether or not such arrangement, understanding or action is formal or in writing. In view of this, transaction of sale of furnishing would amount to a transaction.

Example 2: –

ICO manufactures shirts and trousers (in-house) for its showroom of readymade garments. FCO agrees to supply fine quality of fabric as demanded by ICO, on a no-return, full upfront payment basis, without any formal agreement. FCO supplied sub-standard quality of fabric due to which ICO suffered heavy losses. Would the transaction of sale of fabric amount to a Transaction , even though there is no formal agreement between parties ?

Solution : –

To constitute a transaction for Transfer Pricing purpose, it is not mandatory to have a formal written agreement, or any intention of the parties to legally enforce a transaction. However, to constitute a Transaction, there should be an arrangement, understanding or action between parties. In the present case, even though there was no formal agreement, there was an understanding between parties that FCO would supply fine quality of fabric as demanded by ICO. In view of this, transaction of “sale of fabric” would amount to a transaction for Transfer Pricing purposes.

Definition of International Transaction – Section 92B of Income Tax Act

In order to constitute an International Transaction, a transaction should satisfy the following conditions : –

- It should be a transaction as defined in Section 92F,

- Transaction should be between two or more Associated enterprises.

- Either one, or both the parties /AE’s to transaction should be non-residents.

- Transaction should relate to any of the following :

- Purchase, sale or lease of tangible or intangible property; or

- Provision of services; or

- Lending or borrowing money; or

- Any other transaction having a bearing on the profits, income, losses or assets of the enterprises; or

- Mutual agreements or arrangements between two AE’s for allocation or apportionment of, or any contribution to, any cost or expense incurred or to be incurred in connection with a benefit, service or facility provided or to be provided to any one or more of such enterprises.

Case Law – Receipt of security premium below market value in respect of issue of shares – Whether an International Transaction?

Vodafone India Services (P.) Ltd. v Union of India [2014] 50 taxmann.com 300 (Bombay)

Facts: –

Vodafone India (‘Assessee’) issued 2,89,224 shares [face value of Rs. 10 each] at a premium of Rs. 8,509 per share to its holding company. It had determined the fair market value of equity shares at Rs. 8,519 per share. However, according to Assessing Officer and TPO, the assessee ought to have valued each equity share at Rs. 53,775. Accordingly, shortfall in premium to the extent of Rs. 45,256 per share (Rs 53,775 – Rs 8,519) was treated as income of the assesse by the AO and TPO to the extent of shortfall of receipts of Rs. 1308.91 crores.

Held : –

- The activity of issue of shares to Associated enterprise at a price below the fair market value does not give arise to any income. There should be income arising from International Transaction for application of Transfer Pricing provisions.

- Income will not include capital receipts , unless such receipts are specifically specified to be covered as income.

- The amounts received on issue of share including the premium is on capital account. Thus, receipt of security premium from Associated Enterprise below market value could not be considered as international transaction.

- Thus, Transfer Pricing provision are not applicable on such transaction.

CBDT’s instruction No. 2/2015, dated 29-1-2015

CBDT had also accepted the aforesaid judgment of Bombay High Court that premium on issue of shares, was on capital account and does not give rise to any income. Thus, premium on issue of shares not liable to Transfer Pricing adjustment.

EXAMPLES ON INTERNATIONAL TRANSACTION – SECTION 92B OF INCOME TAX ACT

Example 1 : –

A Ltd. (India), purchases raw material from its Associated enterprise AB Ltd. (India). Would the transaction amount to an international transaction ?

Solution : –

In order to be considered as international transaction, one of the party to the transaction should be non-resident. In this case, neither A Ltd. nor AB Ltd. is non-resident. Thus, such transaction would not be considered as an international transaction. Such transaction may be covered as “Specified Domestic Transaction” where one of the entity is claiming profit linked deductions, i.e., Section 80-IA, 80-IB, 10A, etc. or other conditions applicable on SDT are satisfied.

Example 2 : –

D Ltd. (India) imports goods from E International (Switzerland). D Ltd holds 10% shares in E International. Would the transaction amount to an international transaction?

Solution : –

In order to be considered as international transaction, both parties should be Associated enterprise.

In this case, D Ltd. is holding less than 26% shares in E International. Thus, D Ltd. and E International are not Associated enterprise. Accordingly, such transaction of import would not be considered as an international transaction.

Example 3 : –

C Ltd. (India) imports 10,000 units of goods from its Associated Enterprise C International (Germany) at USD 50 per unit. C Ltd. (India) imports 10,000 units of goods of same quality from independent third party in Germany at USD 50 per unit. Whether the transaction is at arm’s length price ? Would the transaction amount to an international transaction?

Solution : –

In this case, the transaction of import from Associated enterprise is at arm’s length price as C Ltd. imports same quality of goods from third party at USD 50 per unit.

Transaction of import from Associated enterprise would be considered as an “international transaction” even if transaction of import is made at arm’s length price.

Example 4 : –

V (India) is an Associated enterprise of V International (UK). It issued certain shares at Rs. 5,000 per share (face value of Rs. 10 each and a premium of Rs. 4,990 per share) to V International. The market value of per share determined by TPO was Rs. 10,000 per share.

Whether the receipt of premium at less than the FMV would be deemed as an international transaction ?

Solution : –

Receipt of lower premium on issue of shares to an Associated enterprise, would not be considered as an international transaction as per the Ruling of Bombay High Court in case of Vodafone and CBDT’s instruction No. 2/2015, dated 29-1-2015.

Deemed International Transaction [Section 92B of Income Tax Act] (2)

In certain cases, to avoid applicability of TP provisions, AE’s may agree into a transaction, by adding an independent third party to a transaction, such that TP provisions would not apply, if the form in which the transaction takes place is considered . However, in substance, the terms and conditions relating to such transactions are decided by the Associated Enterprise in such a manner, as if the transaction was between two Associated Enterprises. To deal with such cases the concept of deemed International transaction has been Incorporated under the Transfer Pricing laws.

Let us say there are two AE’s A and B . Transaction entered into by an enterprise (A), with a person other than an Associated enterprise (C) (i.e., independent third party) shall be deemed to be a transaction between two AEs (A and B) , if :

- there exists a prior agreement in relation to the relevant transaction between independent third party (C) and the AE (B); or

- the terms of the relevant transaction are determined in substance between independent third party (C) and the AE (B) ;

Note : –

The above provision shall apply where either the enterprise itself (A) , or its Associated enterprise (B), or both are non-resident ( A and B) , irrespective of the fact whether the independent third party (C) is a non-resident or not. Further, it should be noted that where the nature and purpose of relevant transaction, is completely different from what was contemplated in the prior agreement between AE and third party, this clause shall not be applicable.

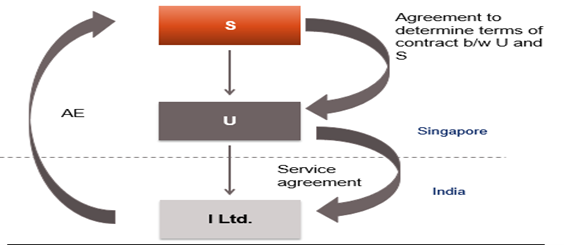

Facts:

- I Ltd. of India is a wholly owned subsidiary of S International of Singapore .

- I Ltd. and U International , Singapore, an independent third party, enter into an agreement for provision of services by U International . Terms of agreement relating to pricing, discount, quantity and date of supply between I Ltd. and U International will be governed by prior agreement between S International and U.

Issue:

Whether the transaction between I Ltd. and U International would be deemed as an international transaction ?

Diagram 1.35

The transaction between I Ltd. and U International would be deemed as an international transaction because of prior agreement between U and S International.

Example 2 : –

In the above example, if the nature and purpose of the transaction between I Ltd. and U International is entirely different from what was contemplated in the prior agreement between S and U Ltd., whether the transaction between I Ltd. and U International would be deemed as an international transaction ?

Solution : –

Transaction between I Ltd. and U International cannot be deemed as international transaction in such a case, as the nature and purpose of relevant transaction is completely different from what was contemplated in the prior agreement between U Ltd. and S International.

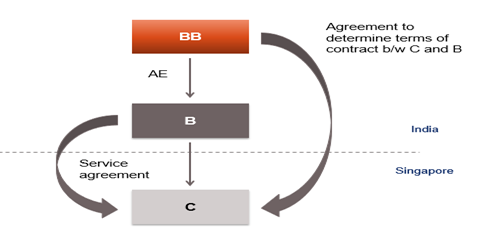

Diagram 1.36

Facts:

BB Ltd. and B Ltd. of India are under the common management and control of BBB India Private Limited. BB Ltd. entered into an agreement with C international (non AE) to determine the terms of provision of services between C International and B Ltd. B Ltd. and C International enter into a service agreement for provision of services.

Issue:

Whether the transaction between B Ltd. and C International would be deemed as an international transaction ?

Solution:

For an international transaction, one of the AE should be non-resident. In this case neither B Ltd. nor BB Ltd. are non-resident. Hence, the transaction between B Ltd. and C International cannot be deemed as international transaction.

Explanation to Section 92B of Income Tax Act – International Transaction

The definition of the term ‘international transaction’ also includes several other items including tangible/ intangible property.

| International Transaction shall include | Property/ Assets covered | |

| Tangible property |

• Purchase of Tangible property |

Tangible property covers : –

• Machinery |

| Intangible Property

|

• Purchase of Intangible Property • Sale Intangible Property • Transfer Intangible Property • Lease Intangible Property • Use Intangible Property |

Intangible property covers : –

• Patents |

| Rights

|

• Transfer of ownership rights • Provision of use of certain rights |

Rights may relate to any of the following assets ; – • Trademark • Franchises • Know-how • Any other business or commercial rights of similar nature • Customer List • Marketing Channel, brand, commercial secret • Exterior design or practical and new design |

| International Transaction shall include | Transaction relates to |

| Capital financing | • Long-term or short-term borrowings • Lending • Guarantee • Purchase or sale of marketable securities • Any type of Advance • Payments or deferred payments • Receivable • Any other debt arising during the course of business |

| Provision of services | • Scientific research

• Market development • Technical service • Market research • Design • Consultation • Marketing management • Legal or accounting service • Administrations • Repairs |

| Transaction of business restructuring or reorganization, entered into by an enterprise irrespective of the fact that it has bearing on:

• Profits of such enterprise at the time of transaction or at any future date |

Merger of Foreign AE into Indian Company |

| Marketing related intangibles

|

• Logos • Trademarks • Brand names • Trade names |

| Technology related intangibles

|

• Technical documentation such as laboratory notebooks • Process patents • Technical know-how • Patent applications |

| Artistic related intangibles

|

• Musical composition • Copyrights • Literacy works and copyrights • Engravings • Maps |

| Customer related intangibles | • Customer relationship • Open purchase orders • Customer contracts • Customer list |

| Contract related intangibles | • Favorable supplier • Contracts • License agreements • Franchise agreements • Non-compete agreements |

| Engineering related intangibles

|

• Blueprints • Industrial design • Proprietary documentation • Product patents • Trade secrets, Engineering drawings and shematics |

| Data processing related intangibles

|

• Software copyrights • Proprietary computer software • Automated database • Integrated circuit masks and masters |

| Human capital related intangibles | • Union contracts • Employment agreements • Trained and organised workforce |

| Location related intangibles | • Mineral exploitation rights • Leasehold interest • Air rights • Water rights |

| Goodwill related intangibles

|

• Personal goodwill of professional • Professional practice goodwill • Institutional goodwill • Celebrity goodwill • General business going concern value |

| Others | • Programmes • Technical data • Estimates • Systems • Surveys • Procedures • Studies • Methods • Forecasts • Campaigns • Customer list |

| Any Other similar item that derives its value from its intellectual content rather than its physical attributes |

For any queries, please write them in the Comment Section or Talk to our tax expert