Other Method Transfer Pricing

Although the methods that have been explained in details in the previous articles have provided for situations that may arise while engaging in transactions with Associated Enterprises, there may be instances that cannot be covered under any of the previous-mentioned methods. As a result the Central Board of Direct Taxes introduced Rule 10AB (Other Method Transfer Pricing) to the Income Tax Rules, 1962 to broaden the scope of ALP Principle. Given below is a brief overview of Rule 10AB- Other Method Transfer Pricing.

| Principle of International Taxation | Transfer Pricing |

| Transaction between | International Parties |

| Transfer Price | Price charged between two Associated Enterprises |

| Arm’s Length Price Principle | Price charged between two unrelated parties |

| Governing Provision | Rule 10AB, Income Tax Rules, 1962 |

| Factors to be considered for application of method |

|

| Elements in the consideration of an appropriate method |

|

| Application of method | Any method that takes into account:

|

CBDT has prescribed the Other Method Transfer Pricing by inserting Rule 10AB to the Income-Tax Rules. For determination of arm’s length price in relation to international transaction, the “Other Method’ shall be any method which takes into account the price which has been charged or paid, or would have been charged or paid, for the same or similar uncontrolled transaction, with or between Non-Associated enterprises, under similar circumstances, considering all the relevant facts.

Following points are relevant in order to apply “Other Method” : –

- Characteristics of the property transferred , or services provided;

- Functions performed by the respective parties to the transactions, taking into account taking the asset employed or to be employed, and the risks assumed;

- Formal / written contractual terms of transactions, laying criterion for how responsibilities, risks and benefits are to be divided between parties to the transactions;

- Market condition impacting respective parties to the transactions like geographical location, market size, prevalent laws, level of competition, wholesale/ retail market etc.

Some of the cases where the “Other Method” can be used are as under : –

- Reimbursement of expenses to Foreign Parent or Associated Enterprise ;

SELECTION OF TESTED PARTY

There are various participants in an international transaction. For example, In a transaction of purchase and sale of goods, there is a purchaser and the seller. When we need to compare this transaction, with an independent uncontrolled transaction, one of the parties has to be selected (i.e, either the purchaser or the seller) for the purpose of comparison with another party performing similar functions in an independent transaction. The party in the controlled related party transaction, which is being compared is known as the Tested party. In order to find comparable for a transaction, one of the participant is selected as “tested party”.

Since we need to find comparable for the tested party, when making a decision on which party in the transaction should be chosen for comparison, the following aspects are considered for the tested party : –

- Whether profitability/ pricing , of the tested party can be verified based on most appropriate data ; and

- The data requires reasonable adjustments, for which reliable data can be located.

The party which is generally chosen as the Tested Party : –

- Should be “least complex” amongst the given parties. For example , in case of a BPO company providing call centre services to a manufacturing entity, the BPO entity would have least complex operations and would therefore be the Tested Party ; and

- Should not own valuable intangible property. If the party owns valuable intangible, it would be difficult to find comparable owning similar valuable intangible and hence comparison may not be viable. For example, for TP study of Apple Inc., which owns valuable intangibles, a local 4G Mobile manufacturer would not be an ideal comparable, if the local manufacturer does not own any valuable intangibles.

SELECTION OF PROFIT LEVEL INDICATOR

A profit level indicator (“PLI”) is a measure of a company’s profitability, with respect to a particular Base. They are ratios, that measure relationships between profits of the company and cost incurred, or profits of the company and resources employed (for example Total Asset). These ratios of a company are thereafter used for the purpose of comparison with similar ratios in an uncontrolled transaction.

Since ratios of profit of the company, are a function of denominator, it is important that the denominator should have an untainted base i.e. it should not be received from an AE/ paid to an AE (i.e it should be from uncontrolled or independent transactions) .

For example, if the profits of a company providing IT support services are compared with revenue, the revenue from IT support services, provided by an Indian company to a US subsidiary company, will be tainted because it is received from related party and would not be considered in denominator. So, the PLI, in the above case, should be costs.

| Particulars | Calculations |

| Return on Assets (ROA) | Operating Profit

Operating assets (normally only tangible assets) |

| Return on Capital Employed

(ROCE) |

Operating profit

Capital employed (Total assets – (Cash + Investments))* |

| Return on Cost of Goods Sold | Gross Profit

Cost of goods sold |

| Berry Ratio | Gross Profit

Operating expenses |

| Operating Margin (OM) | Operating Profit

Sales |

| Return on Total Costs (ROTC) | Operating Profit

Total costs |

NOTE : –

*Johnson Matthey India (P.) Ltd. Vs Deputy Commissioner of Income-tax ([2016] 380 ITR 43 (Delhi)) – Return on Capital Employed (“ROCE”) as a PLI would be reliable if there is similarity in composition of assets/capital deployed (and their valuation) by tested party with that of comparables.

SELECTION OF MOST APPROPRIATE METHOD – RULE 10C

In terms of the provision of Rule 10C, the most appropriate method shall be the method : –

- Which is best suited to facts and circumstances of each particular international transaction [or specified domestic transaction]. In other words, the most appropriate method would need to be ascertained for each and every transaction separately; and

- Which provides the most reliable measure of an arm’s length price in relation to the international transaction [or the specified domestic transaction).

FACTORS TO BE CONSIDERED TO SELECT MOST APPROPRIATE METHOD – RULE 10C(2)

Following factors should be taken into consideration in determining the most appropriate method : –

- Nature and class of the international transaction (or specified domestic transaction). Depending on the nature of transaction, the choice of most appropriate method has to be made. The most appropriate method would be different for purchase of goods or provision of services.

- Class of AEs entering into the transaction, and the functions performed by them, taking into account assets employed and risks assumed.

- Availability, coverage and reliability of data necessary for application of the method. There should be sufficient data available to apply a particular method. If data is not available, such method should be avoided.

- Degree of comparability existing between the international transaction (or specified domestic transaction) and the uncontrolled transaction, in terms of quality of products etc ;

- Degree of comparability existing between the enterprises entering into such transactions.

- Extent to which reliable and accurate adjustments can be made to account for differences, if any, between the international transaction (or specified domestic transaction) and the comparable uncontrolled transaction

- Extent to which reliable and accurate adjustments can be made to account for differences, if any, between the enterprise entering into such transactions.

- Nature, extent and reliability of assumptions required to be made in application of a method.

NOTE : –

The onus of selecting the most appropriate method to determine the ALP is on the taxpayer. The taxpayer should demonstrate the correctness of its choice with supporting records and data, irrespective of the fact as to whether, the statute specifically requires him to do or not. However, the Revenue Authorities are at their discretion to accept a particular method based on the nature of transaction.

CATEGORISATION FOR SELECTION OF MOST APPROPRIATE METHOD

As per ICAI’s guidance note following broad categorization should be used for selection of Most Appropriate Method (‘MAM’).

DATA TO BE USED FOR ANALYZING COMPARABILITY OF AN UNCONTROLLED TRANSACTION WITH AN INTERNATIONAL TRANSACTION

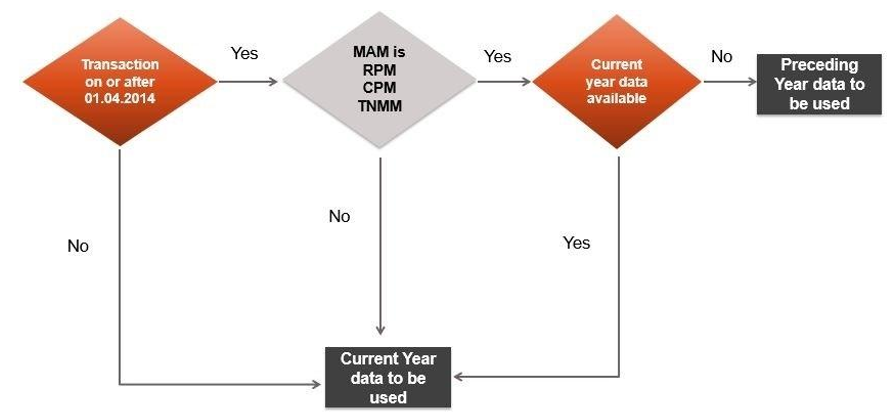

DIAGRAM 1.46

Related party transaction are to be compared with independent transaction. For this purpose, one needs to find comparable data for similar transaction. The data to be used for analyzing comparability of an uncontrolled transaction with an international transaction shall depend on whether the transaction was undertaken before 1.4.2014 or on or after 1.4.2014. Let us look at these two situations in detail : –

A. TRANSACTION BEFORE 01.04.2014

For Transaction before 01.04.2014, in order to compare an international transaction or specified domestic transaction with an uncontrolled transaction, the data to be used in analysing comparability shall be the data relating to the current year in which the international transaction has been entered into. For example, for analysis for FY 2012-13, the comparable transactions that shall be used shall be the one entered into during FY 2012-13.

B. TRANSACTION After 01.04.2014

The transactions, which are entered into after 1.4.2014, can be broadly divided into the following two categories : –

- Most appropriate method for determination of ALP of an international transaction or specified domestic transaction is RPM or TNMM or CPM ; or

- Most appropriate method for determination of ALP of an international transaction or specified domestic transaction is CUP, PSM or Other Method.

MAM is RPM or TNMM or CPM

Where the most appropriate method for determination of ALP of an international transaction or specified domestic transaction, entered into on or after 1.4.2014 is

- Resale price method ; or

- Cost plus method ; or

- Transactional net margin method.

then, the data to be used for analyzing the comparability of an uncontrolled independent transaction with an international transaction shall be as under –

- Current year data Available – The data relating to the current year ; or

- Current year data not Available – In certain cases, current year data may not be available since the companies may not have filed it with the Minsitry of Corporate Affairs. In such a case, the data relating to the financial year immediately preceding the current year, has to be used .

However, where current year data is subsequently available at the time of any assessment proceedings, then, such current year data shall be used for such determination, irrespective of the fact that the data was not available at the time of furnishing the return of income.

MAM is not the Resale price method, or Cost plus method, or Transactional net margin method

Where the most appropriate method for determination of ALP of an international transaction or specified domestic transaction, entered into on or after 1.4.2014 is not the Resale price method, or Cost plus method, or Transactional net margin method, the data to be used shall be the current year data.

WHERE MORE THAN ONE PRICE IS DETERMINED [SECTION 92C] – FROM 01.04.2014 ONWARDS

Summarised chart of the provisions

If the price determined by the application of Most Appropriate Method is a single price, the same is to be applied.

However, if there are more than one price which are arrived at by the application of Most Appropriate Method, the ALP is to be computed : –

- In terms of the range concept, if certain conditions are satisfied; or

- As Arithmetic mean of various prices, if the conditions for applicability of range concept are not satisfied.

WHERE MORE THAN ONE PRICE IS DETERMINED [SECTION 92C] – RULE 10CA

Sometimes the application of, most appropriate method may result in more than one price. In such a case the issue that arises is, which of these prices should be considered, i.e, whether the arithmetic mean of these prices should be considered, or which other method should be applied ?

In such a case, the following methodology will be considered : –

- If the range concept is applicable, it shall be applied

- If the range concept is not applicable then, Arm’s Length price shall be taken to be Arithmetic Mean of such prices.

APPLICABILITY OF ARITHMETIC MEAN WHEN MORE THAN ONE PRICE IS DETERMINED

Where the application of, most appropriate method results in more than one price, and the conditions for the applicability of range concept are not satisfied, Arm’s Length price shall be taken to be Arithmetic Mean of such prices. Arithmetic mean can be calculated by computing the average of various prices, which are obtained by the application of the most appropriate method.

In certain cases, the price calculated by application of Arithmetic mean, may be slightly different from the price at which the actual transaction has taken place.

In order to ensure, the Transfer Pricing adjustments are not made in cases where the actual price is not very different from the Arithmetic mean, tax laws provide for a tolerance limit, wherein if the actual price is within the tolerance limit of the Arithmetic mean (higher or lower), no Transfer Pricing adjustments are made.

Tolerance limit in case of Arithmetic Mean – (Notification No. 50/2017 dated 09.06.2017)

In terms of this Notification, actual transaction price would be taken as Arm’s Length Price, where variation (increase or decrease)between the Arm’s length price determined by use of Arithmetic Mean, and actual transaction price does not exceed –

- 1% of actual transaction price – In case of whole sale trading

- 3% of actual transaction price – In case of other business

It may be noted that the variation has to be calculated as a percentage of the actual transaction price and not be Arithmetic mean.

However, the benefit of permissible variation between the ALP price and Transfer price (as per second proviso to section 92C(2)) would not be available in case of transaction with person in Notified Jurisdiction covered under section 94A.

Note : – These provisions are applicable for A.Y. 2017-18 and A.Y. 2018-19.

MEANING OF “WHOLESALE TRADING”

Wholesale Trading refers to an international transaction or specified domestic transaction of trading in goods, which fulfils the following conditions, namely : –

- Purchase cost of finished goods is 80% or more of the total cost pertaining to such trading activities; and

- Average monthly closing inventory of such goods is 10% or less of sales pertaining to such trading activities.

ARITHMETIC MEAN – ALLOWABLE VARIANCE – EXAMPLES

Let us look at a few examples, wherein the arm’s length price has been computed, considering the tolerance limit provided for by the law : –

| Transaction | Actual Price | ALP by use of Arithmetic Mean | Permissible Variance (1% or 3%) | ALP to be taken |

| Wholesale Trading | 100 | 102 | 99 – 101 (1%) | 102 |

| Wholesale Trading | 100 | 102 | 99 – 101 (1%) | 102 |

| Wholesale Trading | 100 | 99 | 99 – 101 (1%) | 100 |

| Other than wholesale trading | 100 | 104 | 97 – 103 (3%) | 104 |

| Other than wholesale trading | 100 | 103 | 97 – 103 (3%) | 100 |

| Other than wholesale trading | 100 | 97 | 97 – 103 (3%) | 100 |

EXAMPLE: –

Zebra Limited, an Indian company , sold certain helmets to Deer Pte Singapore , which is also a Wholly owned subsidiary of its parent Lion BV , Netherlands at Rs. 1,50,000. Various sale price of helmets, determined under CUP method are –

Rs. 1,40,000, Rs. 1,60,000, Rs. 1,70,000, Rs. 1,80,000 and Rs. 1,90,000.

Zebra Limited is not a wholesale trader. Determine the arm’s length price of transaction ?

SOLUTION : –

| Particulars | Amount (Rs.) |

| Arithmetic Mean

[1,40,000+1,60,000+1,70,000+1,80,000+1,90,000]/5 |

1,68,000 |

| Tolerance tag (3% of transaction price) of Rs. 1,50,000 – Note 1 | 4,500 |

| Tolerance limit | 1,45,500 – 1,54,500 |

| ALP of transaction – Note 2 | 1,68,000 |

NOTE 1 : –

Tolerance limit is 1% for wholesale traders and 3% for others. Limit of 3% would be applicable in this case as Zebra Limited is not a wholesale trader.

NOTE 2 : –

ALP of transaction would be the Arithmetic Mean (i.e., Rs 1,68,000) , since it is outside the limit of tolerance (i.e., Rs 1,54,500)

EXAMPLE : –

Kanha Limited, India, sold certain mobile phones to James and Co. UK, a partnership firm which indirectly owns 26% equity stake in Kanha Limited at Rs. 1,50,000. Various sale price of same mobile phones determined under CUP method are –

Rs. 1,30,000, Rs. 1,40,000, Rs. 1,55,000, Rs. 1,60,000 and Rs. 1,70,000.

Kanha Limited is not a wholesale trader. Determine the arm’s length price of transaction ?

SOLUTION : –

| Particulars | Amount (Rs.) |

| Arithmetic Mean

[1,30,000+1,40,000+1,55,000+1,60,000+1,70,000]/5 |

1,51,000 |

| Tolerance tag (3% of transaction price) of Rs. 1,50,000 – Note 1 | 4,500 |

| Tolerance limit | 1,45,500 – 1,54,500 |

| ALP of transaction – Note 2 | 1,50,000 |

NOTE 1 : –

Tolerance limit is 1% for wholesale traders and 3% for others.

Limit of 3% would be applicable in this case as Kanha Limited is not a wholesale trader.

NOTE 2 : –

ALP of transaction would be the actual transaction price of Rs 1,50,000 as Arithmetic Mean (i.e., Rs 1,51,000) is within the limit of tolerance (i.e., Rs 1,45,500 – Rs 1,54,500).

APPLICABILITY OF RANGE CONCEPT – WHEN MORE THAN ONE PRICE IS DETERMINED

Where more than one price are determined by use of Most Appropriate Method, the Range concept is applicable when all of the following conditions are satisfied. Failure to satisfy any one of the aforesaid conditions would result in non-applicability of range concept. : –

- Transaction is undertaken on or after April 1, 2014 ;

- Arm’s length price is determined by use of either of the following methods : –

- Transactional Net Profit Method (TNMM), or

- Comparable uncontrolled price Method (CUP Method), or

- Cost Plus Method (CPM), or

- Resale Price Method (RPM).

- Range concept is not applicable when either Profit Split Method or other method (given under Rule 10AB) is used to determine the Arm’s length price.

- Six or more comparables are available in the dataset.

The decision tree of the concept is as under : –

(I) APPLICATION OF RANGE CONCEPT – WHEN DATA OF SINGLE YEAR IS USED

Once the range concept is applicable, one needs to find out whether the data which is available for comparison is for a single year, or for more than 1 year ?

APPLICATION OF RANGE CONCEPT – WHEN DATA OF SINGLE YEAR IS USED

In such a case, the range concept has to be applied as under : –

STEP 1: –

Dataset of Prices or Profit margins should be arranged in Ascending order.

STEP 2: –

Determine 35th Percentile of the given dataset .

STEP 3: –

Determine 65th Percentile of the given dataset.

STEP 4: –

Arm’s length range will begin from 35th Percentile and end on 65th Percentile.

STEP 5 : –

Actual transaction price or profit margin would be accepted if it falls in this range of 35th-65th percentile and accordingly, no Transfer Pricing adjustment would be required in this case.

STEP 6 : –

However, if actual transaction price or profit margin is outside the range of 35th-65th percentile, Median of dataset would be computed, and it would be taken as arm’s length price

EXAMPLE 1 : –

In the given case, at the time of application of range concept, the data of SINGLE YEAR IS available for a dataset of 7 prices , which when arranged in Ascending order is as under : –

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | |

| Price (Rs. in Thousands) | 42 | 43 | 44 | 45 | 46 | 47 | 48 |

Determine the Range ?

SOLUTION : –

| 35th Percentile | [Number of items in dataset X 0.35 ] | 7 * 0.35 = 2.45 |

| 65th Percentile | [ Number of items in dataset X0.65] | 7 * 0.65 = 4.55 |

| Value of 35th Percentile | 2.45 is not a whole number. Value of next higher data (i.e., 3) shall be taken | 44 |

| Value of 65th Percentile | 4.55 is not a whole number. Value of next higher data (i.e., 5) shall be taken | 46 |

| Range | 35th – 65th Percentile | 44,000 – 46,000 |

EXAMPLE 2 : –

In the given case, at the time of application of range concept, the data of SINGLE YEAR IS available for a dataset of 20 prices , which when arranged in Ascending order is as under : –

| S. No. | Profits (Rs. in Thousands) | S. No. | Profits (Rs. in Thousands) |

| 1 | 42.00 | 11 | 48.45 |

| 2 | 43.00 | 12 | 48.48 |

| 3 | 44.00 | 13 | 48.50 |

| 4 | 44.50 | 14 | 49.00 |

| 5 | 45.00 | 15 | 49.10 |

| 6 | 45.25 | 16 | 49.35 |

| 7 | 47.00 | 17 | 49.50 |

| 8 | 48.00 | 18 | 49.75 |

| 9 | 48.15 | 19 | 50.00 |

| 10 | 48.35 | 20 | 50.15 |

Determine the range ?

SOLUTION : –

| 35th Percentile | [Number of items in dataset X0.35] | 20 * 0.35 = 7 |

| 65th Percentile | [Number of items in dataset X0.65] | 20 * 0.65 = 13 |

| Value of 35th Percentile | 35th Percentile place (i.e., 7) is a whole number. Thus, Average of prices at 7th and 8th place will be taken | (47 + 48)/ 2 =

Rs. 47,500 |

| Value of 65th Percentile | 65th Percentile place (i.e., 13) is a whole number. Thus, Average of prices at 13th and 14th place will be taken | (48.5 + 49)/ 2 =

Rs. 48,750 |

| Range | 35th – 65th Percentile | Rs. 47,500 – 48,750 |

EXAMPLE : –

Considering the facts of earlier example, determine the Arm’s Length Price in following scenarios : –

- Actual Transaction Price is Rs. 48,000 ?

- Actual Transaction Price is Rs. 45,000 ?

SOLUTION : –

In the first scenario, the Actual transaction price of Rs 48,000 is within the range. Thus, Arm’s length price would be the actual transaction price, i.e., Rs 48,000.

In the second scenario, the actual transaction price of Rs 45,000 is outside the range of Rs 47,500-48,750. Thus, median of dataset would be computed to determine the arm’s length price.

Median of Dataset

20 X 0.50 = 10

Since, 10 is the whole number, median will be the average of the value at 10th and 11th place.

(48.35 + 48.45)/2 = 48.40

Arms’ length price of transaction would be the Median of dataset, i.e., Rs 48,400.

(II) RANGE – APPLICATION OF MULTIPLE YEAR DATA FOR CONSTRUCTION OF DATASET

The uncontrolled independent transaction, will be identified based on the current year data, while in some cases, it may be identified based on data of previous year.

The application of multiple year data for construction of dataset, would differ, depending on whether the uncontrolled transaction has been identified on the basis of current year data, or data of previous year.

This has been discussed in the subsequent paragraph : –

Transaction identified on the basis of Current year data : –

Let us say Company A sold certain goods to Company B, an Associated Enterprise, during financial year 2019-20. Similar transaction was also undertaken by company C during financial year 2019-20, which was identified as a comparable uncontrolled transaction. In the light of this background, let us evaluate the applicability of these provisions : –

Conditions when the Range concept and multiple year data has to be used for Construction of Dataset –

- The most appropriate method should be either of the following : –

-

- Resale price method, or

- Cost plus method, or

- Transactional net margin method ; and

- The comparable uncontrolled transaction should be identified on the basis of data relating to the current year (in the given example, similar transaction was also undertaken by company C during financial year 2019-20, i.e during the current year) ; and

- The enterprise undertaking the said uncontrolled transaction ( Company C), has in either or both of the two immediately preceding financial years, undertaken the same or similar comparable uncontrolled transaction. For example, in the given facts, this provision would be applicable where Company C, also had similar transaction during financial year : –

- 2018-19 and not in 2017-18;

- 2017-18 and not in 2018-19;

- 2017-18 and 2018-19;

- If all the above conditions are satisfied, then the following shall be carried out : –

-

- Most appropriate method used in the current year (FY 2019-20) shall be applied in similar manner to the comparable uncontrolled transaction or transactions undertaken in the aforesaid period (either of the 3 periods discussed above) and the price in respect of such uncontrolled transactions shall be determined (for Company A) ; and

- Weighted average of the prices, of the comparable uncontrolled transactions undertaken in the current year and in the aforesaid period (either of the 3 periods discussed above) preceding it shall be included in the dataset.

EXAMPLE : –

AE 1 has sold coffee beans to AE 2 in F.Y. 2019-20.

Non-AE has sold the similar coffee beans to Non-AE 1 in F.Y. 2017-18, 2018-19 and 2019-20.

Determine which year data should be considered to compute the range under TNMM ?

SOLUTION : –

In order to determine the range under Transactional Net Margin Method, the weighted average profit margin of F.Y. 2017-18, 2018-19 and 2019-20 of Non-AE should be considered.

RANGE – NON-INCLUSION OF PRICE OF UNCONTROLLED TRANSACTIONS IN THE DATASET

However, it should be kept in mind, that when the data used to arrive at the ALP is relating to the current year (say FY 2019-20) , and subsequently at the time of assessment it is established that : –

- The enterprise has not undertaken same or similar uncontrolled transaction during the current year; or

- The uncontrolled transaction undertaken by an enterprise in the current year is not a comparable uncontrolled transaction , i.e, there were no internal comparable transaction undertaken by the company,

then, irrespective of the fact that such an enterprise had undertaken comparable uncontrolled transaction in the any of the immediately preceding two financial years (F.Y. 2017-18 and 2018-19) , the price of uncontrollable transactions or the weighted average of prices of the uncontrolled transactions undertaken by such enterprise shall not be included in the dataset for computing range.

Transaction identified on the basis of Preceding year data : –

Let us say Company A sold certain goods to Company B, an Associated Enterprise, during financial year F.Y. 2019-20. Similar transaction was also undertaken by company C during financial year 2018-19, which was identified as a comparable uncontrolled transaction. In the light of this background, let us evaluate the applicability of these provisions : –

Conditions when the Range concept and multiple year data has to be used for Construction of Dataset –

- The most appropriate method should be either of the following : –

-

- Resale price method, or

- Cost plus method, or

- Transactional net margin method, and

- The comparable uncontrolled transaction should be identified on the basis of data relating to the preceding year (in the given example, similar transaction was undertaken by company C during financial year 2018-19, i.e during the preceding year) ; and

- The enterprise undertaking the said uncontrolled transaction ( Company C) , has in the immediately preceding financial year (FY 2017-18) undertaken the same or similar comparable uncontrolled transaction . In other words, this provision would be applicable where Company C, had similar transaction during financial year 2017-18 and not in 2018-19;

- If all the above conditions are satisfied, then the following shall be carried out as under : –

-

- Price in respect of such uncontrolled transaction shall be determined by applying the most appropriate method in similar manner , as it was applied to determine the price of comparable uncontrolled transaction undertaken in preceding year ; and

- Weighted average of the prices, of the comparable uncontrolled transactions undertaken in the aforesaid period of two years (two years immediately preceding the current year, i.e, 2017-18 and not in 2018-19) shall be included in the dataset.

EXAMPLE : –

AE 1 has sold coffee beans to AE 2 in F.Y. 2019-20.

Non-AE 1 has sold similar coffee beans to Non-AE 2 in F.Y. 2017-18 and 2018-19.

Comparable uncontrolled transaction has been identified on the basis of data relating to F.Y. 2018-19.

Determine the period of range as per TNMM ?

SOLUTION : –

In order to determine the range under Transactional Net Margin Method, the weighted average profit margin of F.Y. 2017-18 and 2018-19 (i.e., preceding two years) should be taken.

RANGE – MULTIPLE YEAR/ SINGLE YEAR DATA

| Method | Applicability of Range | Single Year/ Multiple Year |

| Resale Price Method | Applicable | Multiple year data |

| Cost Plus Method | Applicable | |

| Transactional Net Margin Method | Applicable | |

| CUP | Applicable | Single year data |

| Profit Split Method | Not Applicable | |

| Other Method | Not Applicable |

RANGE– MANNER OF ASSIGNING WEIGHT

The weighted average of the prices shall be computed (in case of multiple year’s data) in following manner : –

| Method | Manner of computing weight price |

| Resale price method | Assign weights to the quantum of sales which has been considered for arriving at the respective prices. |

| Cost Plus Method | Assign weights to the quantum of costs which has been considered for arriving at the respective prices. |

| Transactional Net Margin Method | The weighted average of the prices shall be computed with weights being assigned to the

• quantum of costs incurred, or which has been considered for arriving at the respective prices. |

EXAMPLE : – COMPUTATION OF RANGE

Alpha Limited India, is engaged in the business of providing IT support services to some of its overseas AE’s. It satisfies all conditions relating to the applicability of the Range concept on the related party transactions with foreign AE and the data of comparable uncontrolled transactions/ entities undertaking such transactions, which is available at the time of furnishing return of income for FY 2018-19, reflects that 7 enterprise have undertaken the comparable uncontrolled transaction in the FY 2018-19.

All such enterprises have also undertaken during 2 years preceding current year. The Profit Level Indicator (PLI) used in applying the most appropriate method is Operating profit as compared to operating cost (OP/OC). The weighted average, based upon the weight of OC is as under :

| S. No. | Entity | Year 1 | Year 2 | Year 3 (Current year) | Aggregation of OC and OP | Weighted Average |

| 1 | A | OC = 100

OP = 12 |

OC = 150

OP = 10 |

OC = 225

OP = 35 |

Total OC = 475

Total OP = 57 |

OP/OC = 12% |

| 2 | B | OC = 80

OP = 10 |

OC = 125

OP = 5 |

OC = 100

OP = 10 |

Total OC = 305

Total OP = 25 |

OP/OC = 8.2% |

| 3 | C | OC = 250

OP = 22 |

OC = 230

OP = 26 |

OC = 250

OP = 18 |

Total OC = 730

Total OP = 66 |

OP/OC = 9% |

| 4 | D | OC = 180

OP = -9 |

OC = 220

OP = 22 |

OC = 150

OP = 20 |

Total OC = 550

Total OP = 33 |

OP/OC = 6% |

| 5 | E | OC = 140

OP = 21 |

OC = 100

OP = -8 |

OC = 125

OP = -5 |

Total OC = 365

Total OP = 8 |

OP/OC = 2.2% |

| 6 | F | OC = 160

OP = 21 |

OC = 120

OP = 14 |

OC = 140

OP = 15 |

Total OC = 420

Total OP = 50 |

OP/OC = 11.9% |

| 7 | G | OC = 150

OP = 21 |

OC = 130

OP = 12 |

OC = 155

OP = 13 |

Total OC = 435

Total OP = 46 |

OP/OC = 10.57% |

Calculate the Range ?

SOLUTION : –

| 35th Percentile | [Number of items in dataset * 0.35] | 7 * 0.35 = 2.45 |

| 65th Percentile | [Number of items in dataset * 0.65] | 7 * 0.65 = 4.55 |

| Value of 35th Percentile | 2.45 is not a whole number. Value of next higher data (i.e., 3) shall be taken | 8.2% |

| Value of 65th Percentile | 4.55 is not a whole number. Value of next higher data (i.e., 5) shall be taken | 10.57% |

| Range | 35th – 65th Percentile | 8.2% – 10.57% |

For any queries, please write them in the Comment Section or Talk to our tax expert