UAE Tax Residency Certificate (TRC) – 90 Day Rule: Eligibility, Documents and How to Apply

If you have been physically present in UAE for 90 days or more during a consecutive 12-month period, you may qualify for a UAE Tax Residency Certificate (TRC) under the 90-day rule. This rule applies specifically to individuals who are UAE citizens, UAE residents or GCC nationals and who maintain a permanent place of residence, employment or a business in the UAE.

A UAE TRC enables you to claim benefits under the UAE’s Double Taxation Avoidance Agreements (DTAAs) — including reduced withholding tax on income from India — through the FTA’s EmaraTax portal. Sorting Tax Advisory Services Pvt. Ltd. assists individuals in assessing their eligibility under the 90-day rule, compiling the correct documents and filing a complete, accurate application with the Federal Tax Authority (FTA).

What is the UAE Tax Residency Certificate 90-Day Rule?

The UAE Tax Residency Certificate (TRC) 90-day rule is a specific residency threshold that allows certain individuals to qualify as UAE tax residents even when their UAE presence falls below the standard 183-day threshold.

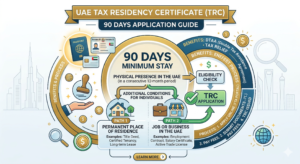

Under Cabinet Decision No. 85 of 2022 on the Determination of Tax Residency [⚠️ see yellow box below], an individual qualifies as a UAE tax resident under the 90-day rule if they satisfy ALL of the following conditions:

Condition 1 — Physical Presence: Physically present in the UAE for 90 days or more (but fewer than 183 days) in a consecutive 12-month period.

Condition 2 — Eligible Status: Must be one of the following:

- UAE national (citizen); or

- UAE resident (valid UAE residency visa); or

- GCC national (citizen of Saudi Arabia, Kuwait, Qatar, Bahrain or Oman)

Condition 3 — UAE Connection: Must also satisfy at least ONE of:

- A permanent place of residence in the UAE; or

- Employment / a job in the UAE; or

- A business in the UAE

Where an individual’s UAE presence exceeds 183 days, residency is established by presence alone — the nationality and connection conditions above do not need to be separately satisfied.

This page focuses specifically on the 90-day rule for individuals. For the 183-day threshold or for corporate TRC applications, see our main

Why Do You Need a UAE TRC (90-Day Rule) ?

A UAE TRC obtained under the 90-day rule serves the same legal purpose as one issued under the 183-day rule. It is an official certificate from the Federal Tax Authority (FTA) confirming your UAE tax residency for a specific 12-month period. It allows you to:

- Claim treaty benefits under UAE DTAAs — including reduced or nil withholding tax (WHT) rates on dividends, interest and royalties received from treaty partner countries such as India, the UK, Singapore and the Netherlands.

- Avoid double taxation — where income may be taxable in both the UAE and another country, a valid TRC enables you to invoke the relevant DTAA and reduce your total tax burden.

- Reduce TDS deductions in India — a UAE TRC, combined with Form 10F and a No PE Declaration, enables Indian payors to deduct TDS at the DTAA rate rather than the higher domestic rate. Without a TRC, the higher domestic TDS rate applies automatically.

- Prove UAE tax residency for compliance purposes — banks, employers, cross-border contract counterparties and regulators increasingly require TRC documentation from UAE-resident individuals.

If you are a UAE citizen, resident or GCC national with between 90 and 183 days of UAE presence and you receive income from India or other treaty countries, obtaining a UAE TRC under the 90-day rule is a critical compliance step.

"With UAE TRC (90-Day Rule)" vs "Without UAE TRC" - Example - India

UAE Tax Residency Certificate – 90 Day Rule: Impact Comparison

| Situation | ✅ With UAE TRC (90-Day Rule) | ❌ Without UAE TRC |

|---|---|---|

| TDS on income from India (e.g. professional fees, royalties) | 10%–15% under the India-UAE DTAA — saving 5–25% per payment | 20%–40% at domestic Indian TDS rates — significantly higher deduction |

| Access to India-UAE DTAA benefits | Full access — TRC is the mandatory proof of UAE tax residency under Article 4 of the DTAA | Treaty benefits cannot be claimed — domestic tax rates apply automatically |

| Filing Form 10F in India | A valid UAE TRC satisfies the TRC requirement in Form 10F — enabling the full India-UAE DTAA claim | Form 10F cannot be completed without a valid TRC — DTAA benefit blocked |

| Withholding tax on dividends, interest and royalties from treaty countries | Reduced WHT rates under UAE DTAAs with 100+ countries — e.g. 10% on interest vs 20–30% domestic rate | Full domestic WHT rates apply in the source country — no treaty relief |

| Double taxation risk | Mitigated — TRC enables formal invocation of applicable DTAA to eliminate or reduce double taxation | High risk — income may be taxed in both the UAE and the source country with no treaty relief available |

| Proof of UAE tax residency for banks and employers | Official FTA-issued certificate — accepted by banks, employers and counterparties in 100+ countries | No official documentation — may be unable to satisfy KYC or compliance requirements |

| No PE Certificate requirement (India-sourced income) | UAE TRC + No PE Certificate together confirm non-taxability in India — enabling Indian payors to deduct TDS at DTAA rate | Without a TRC, the full documentation chain (TRC + Form 10F + No PE) cannot be established |

| Certificate validity | Valid for the specific 12-month period applied for — renewable annually via FTA EmaraTax | No certificate — must pay higher domestic tax or withholding rates for each year without one |

Get Expert Help with UAE TRC

Documents Required for UAE TRC Under the 90-Day Rule

The following documents are required to support an individual UAE TRC application under the 90-day rule:

- Passport — Valid passport of the applicant (coloured scan of all pages).

- Emirates ID — Valid Emirates ID (front and back).

- UAE Visa / Residence Permit

- Immigration Report

- Source of Income Proof

- Proof of Permanent Residence

- Bank Statement — UAE bank statements

Important notes:

- The immigration report must show at least 90 days of presence in the 12-month period being applied for.

- TRC applications cannot cover future periods — the relevant period must have already commenced or concluded.

- Incorrect or incomplete documents are the most common reason for FTA rejection. Sorting Tax reviews your document pack before submission to minimise this risk.

For the full document requirements and checklist, including for companies.

Individual Eligibility for UAE TRC Under the 90-Day Rule

To qualify for a UAE TRC under the 90-day rule, ALL three of the following conditions must be satisfied for the 12-month period being applied for:

Condition 1 — Physical Presence of 90+ Days

The applicant must have been physically present in the UAE for 90 or more days (cumulative) during a consecutive 12-month period. Your immigration report from the ICA will confirm this.

Condition 2 — Eligible Nationality or Residency Status

The applicant must be one of the following:

- UAE national (citizen)

- UAE resident (holding a valid UAE residency visa at the time of the application period)

- GCC national — citizen of Saudi Arabia, Kuwait, Qatar, Bahrain or Oman

Condition 3 — At Least One UAE Connection

The applicant must also satisfy at least one of the following:

- Permanent place of residence in the UAE — an owned or rented residential property serving as their principal place of residence

- Employment in the UAE — active employment with a UAE-based employer under a valid work permit or employment visa during the relevant period

- Business in the UAE — a registered business, active trade licence or freelance permit in the UAE

Who does NOT qualify under the 90-day rule?

- Individuals who are not UAE citizens, UAE residents or GCC nationals.

- Individuals who are UAE citizens, residents or GCC nationals but who do not satisfy any of the three additional conditions (no UAE residence, employment or business).

- Individuals physically present for fewer than 90 days in the relevant period.

If your presence exceeds 183 days, you do not need to satisfy Conditions 2 or 3 — physical presence alone establishes UAE tax residency.

What About Companies? Corporate UAE TRC Eligibility

The 90-day rule applies exclusively to individuals. Companies and other legal entities wishing to obtain a UAE TRC are subject to a separate eligibility framework and are not assessed on the basis of physical presence.

To be eligible for a UAE TRC, a company must:

- Be incorporated or registered in the UAE; and

- Have been in existence for a minimum of three months from the start of the relevant tax period at the time of application.

Free Zone companies are eligible to apply for a UAE TRC. Offshore entities or International Business Corporations (IBCs) with no UAE economic substance may not be eligible.

For a detailed guide to corporate UAE TRC eligibility, the required documents and the application process.

How to Apply for UAE TRC Under the 90-Day Rule: Step-by-Step

- Verify Your Eligibility — Confirm that you meet all three conditions – Sorting Tax can assess your eligibility before you begin.

- Obtain Proof of your stay in the UAE

- Compile Relevant Documents Pack – Sorting Tax reviews your document pack before submission.

- Apply on UAE Government portal – Initiate the TRC Application , Upload Documents and Pay the Submission Fee .

- FTA will review and approve or ask for additional information . If information is incorrect or data is not provided, application may be rejected

Legal Framework Governing UAE TRC – 90-Day Rule

The following legislation and decisions govern UAE tax residency and the issuance of TRCs for individuals applying under the 90-day rule:

- Cabinet Decision No. 85 of 2022 on the Determination of Tax Residency — Defines the criteria under which individuals and legal entities are treated as UAE tax residents, including the 90-day and 183-day physical presence thresholds and the additional qualifying conditions for individuals.

- Ministerial Decision No. 27 of 2023 — Sets out the specific conditions and administrative requirements for the issuance of Tax Residency Certificates by the FTA, including documentation requirements and the application process via EmaraTax.

- Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses (UAE Corporate Tax Law) — Provides the broader UAE tax framework within which TRC applicants operate.

- Article 4 of the India-UAE Double Taxation Avoidance Agreement (DTAA) — Defines “resident” for the purpose of the India-UAE DTAA. A UAE TRC is the primary documentary evidence that an individual is a UAE resident for treaty purposes, enabling access to reduced withholding tax rates on income from India.

- Section 90 of the Indian Income Tax Act, 1961 — Enables Indian payors to apply DTAA provisions — including reduced TDS rates — where a non-resident presents a valid TRC, Form 10F and (where applicable) a No PE Declaration.

UAE TRC 90-Day Rule – Case Studies

Case Study 1: UAE Resident Freelancer Reducing India TDS

Rahul, a UAE-resident software consultant from India, was engaged by an Indian company for a technology project. He had been physically present in the UAE for approximately 105 days during the relevant 12-month period and held a UAE freelance permit issued by a UAE free zone. He satisfied all three conditions under the 90-day rule: UAE presence of 105 days, UAE residency status and an active business in the UAE.

Sorting Tax assisted Rahul in obtaining his immigration report from the ICA, compiling proof of his UAE freelance licence and Ejari-registered tenancy, and filing his TRC application via EmaraTax. Once his TRC was issued, Sorting Tax also assisted him in filing Form 10F and preparing his No PE Declaration — enabling the Indian company to deduct TDS at the DTAA rate of 10% rather than the domestic rate of 20%.

Case Study 2: GCC National Proving UAE Residency for Banking Compliance

Fatima, a Saudi national employed by a UAE-based multinational and residing in an apartment in Abu Dhabi, spent approximately 95 days per year in the UAE. Her bank in Saudi Arabia required official documentary proof of UAE tax residency. Sorting Tax reviewed her situation under the 90-day rule, confirmed she met all three conditions (GCC national, 95 days UAE presence, UAE employment and UAE residence), and assisted her in applying for a UAE TRC via EmaraTax. The certificate was issued within five business days and accepted by her bank as proof of UAE residency.

Conclusion – UAE TRC Under the 90-Day Rule

The UAE TRC 90-day rule provides an important legal pathway to tax residency certification for UAE citizens, UAE residents and GCC nationals who maintain a meaningful connection to the UAE — even where their physical presence is between 90 and 183 days per year. Qualifying under this rule requires demonstrating the minimum physical presence alongside at least one of the prescribed additional conditions: a permanent UAE residence, employment in the UAE or a business in the UAE.

Obtaining a UAE TRC under the 90-day rule enables you to access treaty benefits under the UAE’s extensive DTAA network, reduce withholding tax on cross-border income (including income from India), and satisfy compliance requirements across multiple jurisdictions. The process requires careful preparation of your immigration report, comprehensive documentation of your UAE ties and accurate, complete filing through the FTA’s EmaraTax portal.

Sorting Tax Advisory Services Pvt. Ltd. provides end-to-end assistance with UAE TRC applications — from eligibility assessment and document review through to FTA submission and post-issuance compliance. We also handle the full India-UAE documentation chain: Form 10F, No PE Certificate, India TRC (Form 10FB) and UAE TRC.

Explore our related services:

- UAE Tax Residency Certificate (main guide) — https://sortingtax.com/uae-tax-residency-certificate/

- Form 10F for Non-Residents — https://sortingtax.com/form-10f-income-tax-act-1961-non-resident/

- No PE Certificate — https://sortingtax.com/no-pe-certificate/

- India TRC (Form 10FB) — https://sortingtax.com/tax-residency-certificate-india/

Get Expert Help with UAE TRC for 90 days or more

FAQ - UAE TRC for less than 90 days

1. What is the UAE Tax Residency Certificate 90-day rule?

The UAE TRC 90-day rule is a tax residency criterion that allows individuals who have been physically present in the UAE for 90 days or more — but fewer than 183 days — during a consecutive 12-month period to qualify for a UAE Tax Residency Certificate, provided they also satisfy certain additional conditions: they must be a UAE citizen, UAE resident or GCC national, and they must have a permanent residence, employment or a business in the UAE.

2. Who is eligible for a UAE TRC under the 90-day rule?

Only individuals who are UAE nationals (citizens), UAE residents (holding a valid UAE residency visa) or GCC nationals (citizens of Saudi Arabia, Kuwait, Qatar, Bahrain or Oman) are eligible under the 90-day rule. They must also satisfy at least one of three additional conditions: a permanent place of residence in the UAE, employment in the UAE or a business in the UAE.

3. What is the difference between the 90-day rule and the 183-day rule for UAE TRC?

Under the 183-day rule, an individual establishes UAE tax residency by physical presence alone — no additional conditions regarding nationality, residence, employment or business need to be met. Under the 90-day rule, the applicant must be a UAE citizen, resident or GCC national and must also satisfy one of the three UAE connection conditions. The 90-day rule is not available to individuals who do not belong to these specific categories.

4. Can I apply for a UAE TRC if I have been in the UAE for only 90 days?

Yes, provided you are a UAE citizen, UAE resident or GCC national and you satisfy at least one additional condition — a permanent place of residence, employment or a business in the UAE during the relevant 12-month period. If all conditions are met, you can apply for a UAE TRC for that period via the FTA’s EmaraTax portal.

5. What documents are required for UAE TRC under the 90-day rule?

You will need: (1) a valid passport, (2) Emirates ID, (3) UAE visa or residency permit (if applicable), (4) an immigration report from the UAE ICA confirming 90+ days of UAE presence, (5) proof of source of income in the UAE (employment contract, trade licence etc.), (6) proof of permanent residence in the UAE (tenancy contract or title deed) and (7) UAE bank statements for the last 6 months. Sorting Tax reviews your document pack before submission to minimise the risk of FTA rejection.

6. How do I prove 90 days of UAE presence for TRC purposes?

Your immigration report (entry/exit travel history) from the UAE Federal Authority for Identity and Citizenship (ICA) is the primary evidence of your physical presence in the UAE. This report shows all entry and exit dates and must confirm 90 or more days of UAE presence in the 12-month period being applied for.

7. Does the 90-day rule apply to companies?

No. The 90-day rule applies exclusively to individuals. Companies and other legal entities applying for a UAE TRC are assessed under a separate framework — they must be incorporated in the UAE and have been in existence for at least three months from the start of the relevant tax period. See our main UAE Tax Residency Certificate page for full details of corporate TRC eligibility.

8. Can a GCC national obtain a UAE TRC under the 90-day rule?

Yes. Citizens of Saudi Arabia, Kuwait, Qatar, Bahrain and Oman are explicitly eligible to apply for a UAE TRC under the 90-day rule, provided they have been physically present in the UAE for 90+ days in the relevant period and they also satisfy at least one of the additional conditions: a permanent place of residence, employment or a business in the UAE.

9. What are the FTA fees for a UAE TRC under the 90-day rule?

FTA fees are charged in two stages. A submission fee is payable at the time of filing the application. The balance issuance fee is payable once the FTA approves the application. The exact fee amount depends on whether the applicant is registered under UAE Corporate Tax and whether a printed certificate is required. Contact Sorting Tax for current fee details before filing your application. [⚠️ Verify exact fee amounts with current FTA guidance before publishing.]

10. How long does it take to get a UAE TRC under the 90-day rule?

Typically 3 to 7 business days for a digital TRC after submission of a complete and correct application on EmaraTax. If a printed copy is also requested, allow 7 to 10 business days. Incomplete or incorrectly documented applications will result in delays or rejection. Sorting Tax’s pre-submission document review significantly reduces the risk of rejection.

11. Can I use a UAE TRC (90-day rule) to claim India DTAA benefits?

Yes. A UAE TRC — regardless of whether it was issued under the 90-day or 183-day rule — is the required proof of UAE tax residency for claiming benefits under the India-UAE DTAA. To claim reduced TDS deductions in India, you will also need to file Form 10F and, in most cases, provide a No PE Declaration. Sorting Tax assists with the full India-UAE documentation chain.

12. For which period can I apply for a UAE TRC under the 90-day rule?

You can apply for any completed or ongoing 12-month period during which you satisfied the 90-day presence threshold and the additional eligibility conditions. The FTA does not issue TRCs for future periods that have not yet commenced. The TRC is valid for the specific 12-month period stated in the certificate.

13. What happens if my UAE TRC application is rejected?

If the FTA rejects your application, they will communicate the reason through the EmaraTax portal. Common rejection reasons include insufficient documentation, fewer than 90 days of UAE presence in the relevant period, or failure to satisfy the nationality or UAE connection conditions. Sorting Tax can help you understand the rejection, remedy the documentation and resubmit a corrected application.

14. Do I need a new UAE TRC for each year?

Yes. A UAE TRC is issued for a specific 12-month (tax) period and is not automatically renewed. If you need to claim treaty benefits or prove UAE tax residency for each financial year separately, you must apply for a new TRC for each relevant period through EmaraTax.

15. How does Sorting Tax help with UAE TRC applications?

Sorting Tax Advisory Services Pvt. Ltd., led by CA Arinjay Jain, specialises in international tax for India-UAE cross-border scenarios. We assess your eligibility under the 90-day rule, review your document pack before submission, file your TRC application with the FTA via EmaraTax, and handle the full India-UAE compliance chain — UAE TRC, Form 10F, No PE Certificate and India TRC (Form 10FB). Contact us at +91-9667714335 or contact@sortingtax.com.