Capital Gains to Non Residents Tax in India – Article 13 – Double Taxation Avoidance Agreement

Article 13 – Capital Gains – Double Taxation Avoidance Agreement

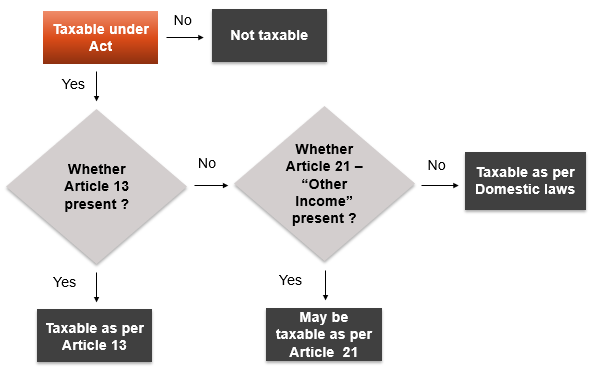

This is the most commonly used Article. It provides for the taxation of income arising from transfer of a capital asset, including transfer of shares. The right to tax income from capital gains may be exclusively with the country of residence, or shared between both the countries.

WHAT COULD BE POTENTIAL SITUATIONS OF CAPITAL GAINS ?

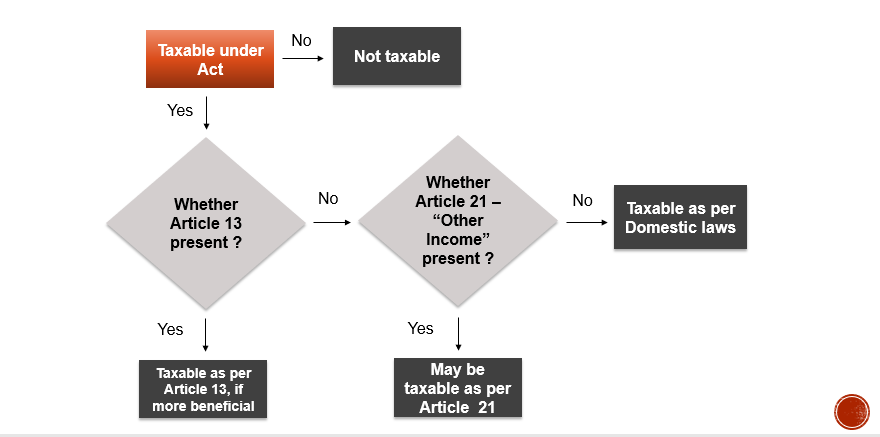

TAXATION OF CAPITAL GAINS

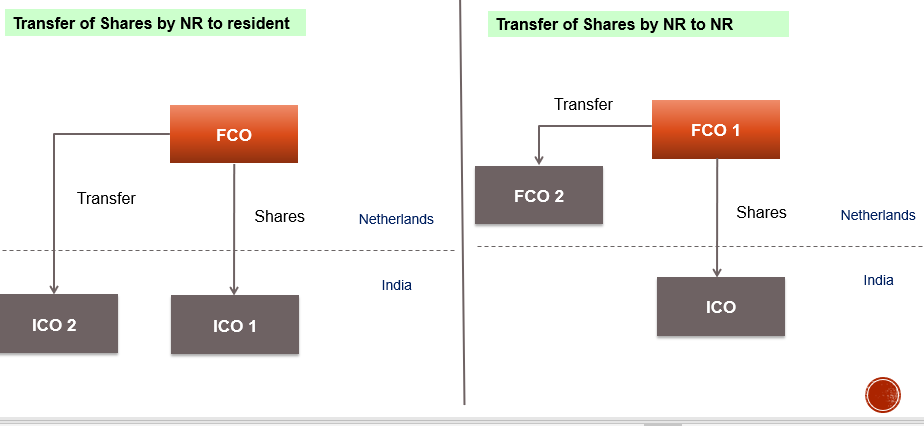

WHAT COULD BE POTENTIAL SITUATIONS WHEN CAPITAL GAINS WOULD ARISE

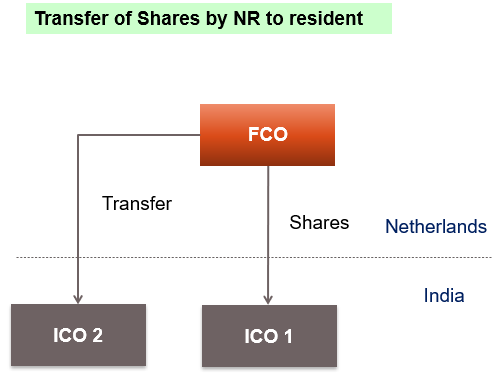

Transfer of Shares by NR to resident

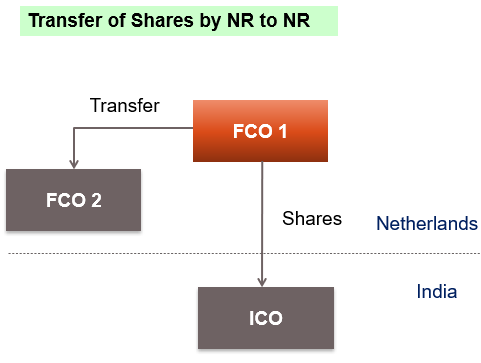

Transfer of Shares by NR to NR

What is the Meaning of “capital gains” ?

1. Term “Capital Gains “ defined under Article 13 ?

2. Article – 3 “General Definitions” requires application of domestic laws to ascertain meaning of terms not defined in Treaty

3. Income assessable under Section 45 of IT Act, 1961, may be considered as Capital gains

4.Subject matter of transfer should be a “Capital assets” and not “stock-in-trade”

5.What if a particular Capital Gains is not taxable under IT Act at all ?

6.Capital gains may be Long-term or Short-term capital gain, and may be chargeable to tax at special or normal rates

Learn More about “Article 13 – Capital Gains Tax” – Subscribe International Tax Course

“CAPITAL ASSETS” COVERED UNDER ARTICLE 13 ?

1. Capital Assets

2. Immovable property referred to in Article 6 – Article 13(1)

3. Movable property forming part of Business property of a PE / Fixed Base – 13(2)

4.Ships, Aircrafts, Boats, etc. operated in international traffic/ movable property pertaining to such operations – 13(3)

5. Shares of Real Estate company – 13(4)

6. Any other property – 13(5)

RIGHT TO TAX OF SOURCE &/OR RESIDENT STATE

Right to tax

- Only India – (No Treaty like Cayman Island)

- Only Treaty Partner (India-Singapore Treaty)

- Both India & Treaty partner (India – USA Treaty)

RIGHT TO TAX WITH TREATY PARTNER – INDIA SINGAPORE TREATY

- Gains derived by a resident of a Contracting State from the alienation of immovable property …..

- Gains from the alienation of movable property forming part of the business property of a permanent establishment …….

- Gains from the alienation of ships or aircraft …….

- Gains derived by a resident of a Contracting State from the alienation of any property other than those mentioned in paragraphs 1, 2 and 3 of this Article shall be taxable only in that State.

RIGHT TO TAX WITH BOTH COUNTRIES – INDIA US TREATY

Except as provided in Article 8 (Shipping and Air Transport) of this Convention

each Contracting State may tax capital gains

in accordance with the provisions of its domestic law.

TAXATION OF CAPITAL GAINS

ALIENATION VS TRANSFER IN CAPITAL GAINS TAX

ALIENATION AS PER INDIA – MAURITIUS TREATY

Alienation means the

sale,

exchange,

transfer, or

relinquishment of the property, or

the extinguishment of any rights therein, or

the compulsory acquisition thereof under any law in force in the respective Contracting States.

Learn More about “Article 13 – Capital Gains Tax” – Subscribe International Tax Course

ALIENATION OF PROPERTY

- Sale of a property

- Exchange of a property

- Extinguishment of rights in a property

- Transfer of a property

- Gift

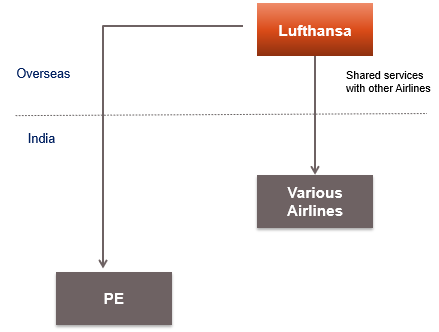

EXISTENCE OF PE AND CAPITAL GAINS TAX – LUFTHANSA GERMAN AIRLINES CASE

Facts:

- Lufthansa airlines provided handling services to other airlines in India, as per the International Airline Technical Pool, as per IATP manual

- It also availed services from other Airlines

- Taxpayer claimed that income from various airline was not taxable in India in terms of Article 8 (4), which covered profits from the participation in a pool.

Issue:

- Whether profits earned by Lufthansa airlines was taxable under Article 8(4) or Article 7 & 5 ?

Held:

- Profits will be taxable under Article 8(4) which specifically covered profit from participation in pool.

ARTICLE 8 AS PER INDIA – GERMANY TREATY

- Profits from the operation of ships or aircraft in international traffic shall be taxable only in the Contracting State in which the place of effective management of the enterprise is situated.

- If the place of effective management of a shipping enterprise is aboard a ship, then it shall be deemed to be situated in the Contracting State in which the home harbour of the ship is situated, or, if there is no such home harbour, in the Contracting State of which the operator of the ship is a resident.

- For the purposes of this Article, interest on funds connected with the operation of ships or aircraft in international traffic shall be regarded as profits derived from the operation of such ships or aircraft, and the provisions of Article 11 shall not apply in relation to such interest.

- The provisions of paragraph 1 shall also apply to profits from the participation in a pool, a joint business or an international operating agency.

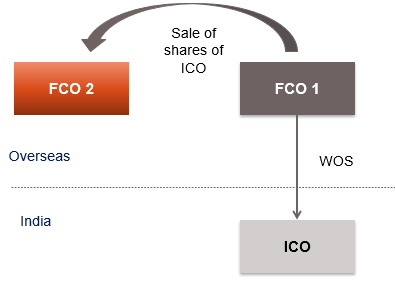

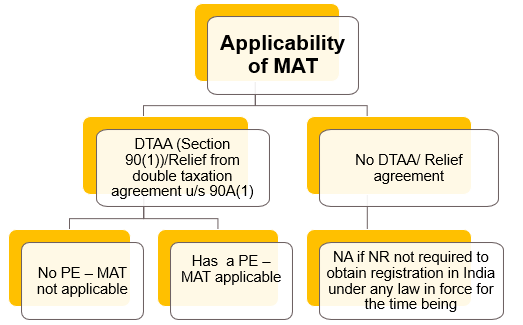

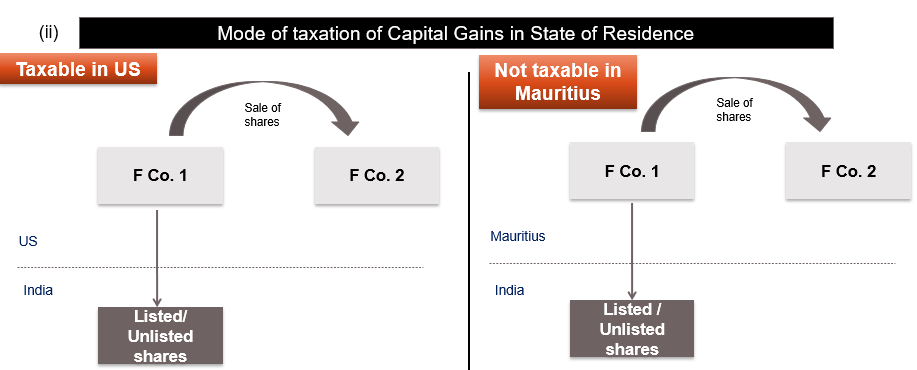

MAT ON SALE OF SHARES OF INDIAN COMPANY

Facts:

- FCO 1 is an Foreign Co. engaged in the manufacturing business

- ICO is a WOS of FCO 1;

- FCO 1 sold shares of ICO to FCO 2, a Mauritius Co.

Issue:

- Whether MAT is applicable on Capital Gain?

Position :

- Explanation 4 to Section 115JB(1) provides that MAT shall not apply to a foreign company if : –

- India has entered into a DTAA (Section 90(1))/relief from double taxation u/s 90A(1) with the country of whom the NR is a resident

- NR does not have a PE in India as per said agreement

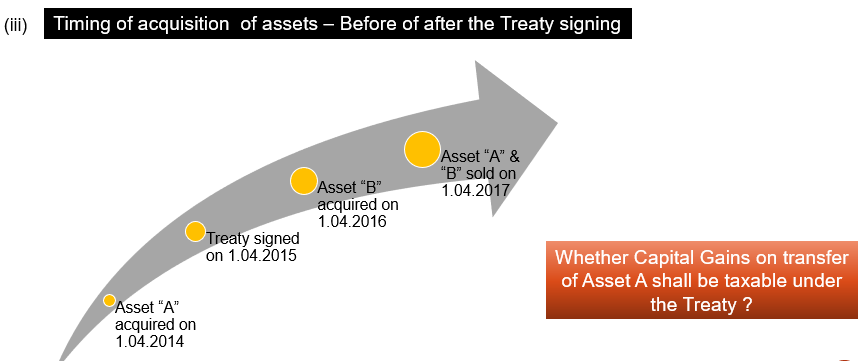

AMENDMENT BY FINANCE ACT 2016

ARTICLE 13(1) – INDIA – AUSTRIA IMMOVABLE PROPERTY

Gains

derived by a resident of Contracting State

from the alienation of a immovable property referred to in Article 6

and

situated in the Other Contracting State

may be taxed in that Other State.

Article 13(1) – Transfer of Immovable Property

Learn More about “Article 13 – Capital Gains Tax” – Subscribe International Tax Course

Article 13(1) – Issues For Consideration

What should be derived ?

Gains (shall include losses)

Who should derive ?

Resident of the other Contracting State

What is the subject matter of transfer ?

Immovable property which is situated in India and referred to in Article 6

Who has the right to tax ?

India also has the right to tax such gains

Article 6 – Immovable Property

“Immovable property” shall have the meaning which it has under the law of Contracting State in which the property in question is situated.

The term shall in any case include property accessory to immovable property, livestock and equipment used in agriculture and forestry, rights to which the provisions of general law respecting landed property apply, usufruct of immovable property and rights to variable or fixed payments as consideration for the working of , or the right to work, mineral deposits, sources and other natural resources;

Ships, boats and aircraft shall not be regarded as immovable property.

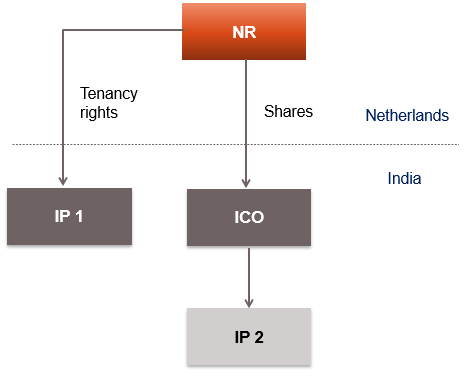

Punnika Parikh – Case Study

Facts:

- Applicant, a citizen of Netherlands, had interest in tenancy rights of a flat in India and ownership of shares in a company having ownership rights in immovable property;

- She wanted to release the tenancy rights and sell shares of the Co.

Issue:

- Whether gains realised from release of tenancy rights & sale of shares are taxable in India ?

Held:

- Gains realised are taxable in India as per DTAA between India & Netherlands, as the property is situated in India.

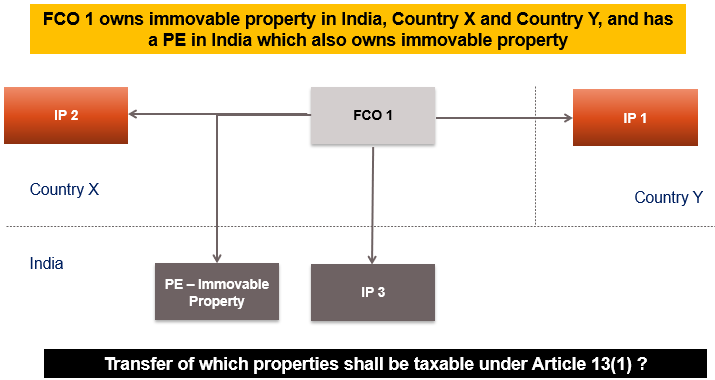

Article 13(2) – India – Austria Treaty – Movable Property of PE Business

Gains from the alienation of movable property

forming part of the business property of a permanent establishment

which an enterprise of a Contracting State has in the other Contracting State or

of movable property pertaining to a fixed base available to a resident of Contracting State in the other Contracting State

for the purpose of performing independent personal services

including such gains from the alienation of such a permanent establishment (alone or with the whole enterprise) or of such fixed base

may be taxed in that other State.

Movable property not forming part of the business property of a permanent establishment shall be taxable as per Article 13 (6)

Application of Article – 13(2)

- Alienation of movable property forming part of business property of a PE

- Alienation of the PE along with such movable property

- Alienation of the whole Enterprise along with the movable property forming part of business property of a PE

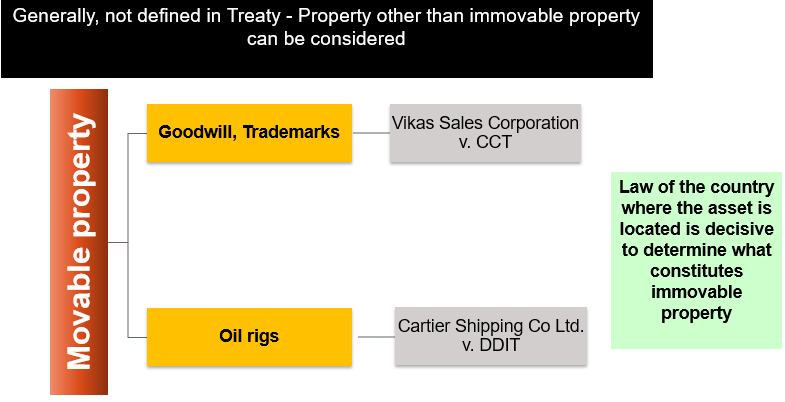

What is Movable Property ?

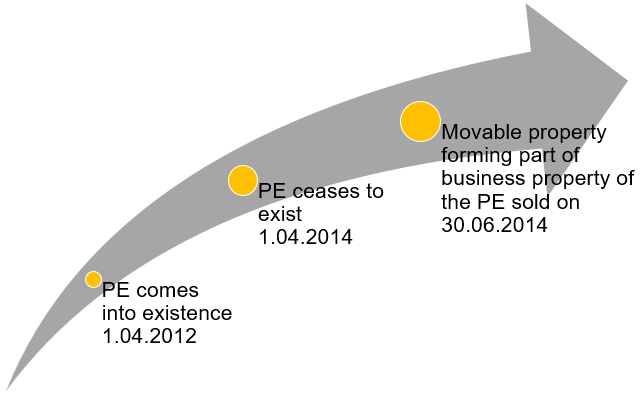

Sale of Capital Asset after Cessation of PE

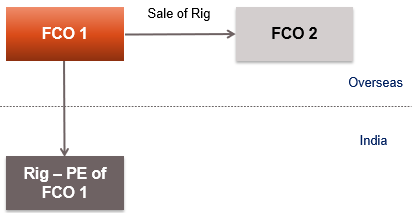

Cartier shipping co. – Alienation of PE

Facts:

- FCO 1 owned a cantilever type jack up rig and the said rig was used for drilling, prospecting and production of hydrocarbons in offshore oil fields;

- FCO 1 sold the said rig to FCO 2 during the relevant assessment year;

- FCO 1 did not disclose the gains realised from sale of said rig.

Issue:

- Whether Capital Gain will be taxable in India ?

Held:

- Gains realised from sale of rig will be taxable in India as per Article 13(2) of India-Mauritius tax treaty.

Since the assessee claimed depreciation on the rig in the past, it was an asset of the PE.

Learn More about “Article 13 – Capital Gains Tax” – Subscribe International Tax Course

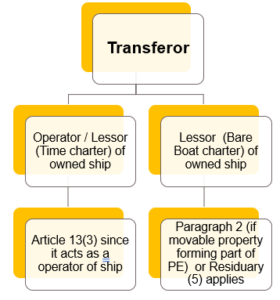

Article 13(3) – India – Netherlands Treaty

Gains from the alienation of ships or aircraft

operated in international traffic

or

movable property pertaining to the operation to such ships, aircraft

shall be taxable only in the Contracting State

in which the place of effective management of the enterprise is situated.

Article 13(3) – Analysis

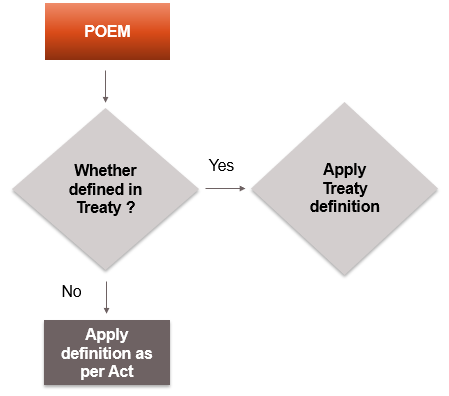

Taxable in the Contracting State in which the Place of effective Management (POEM) of the enterprise is situated

POEM Explanation to Section 6(3)

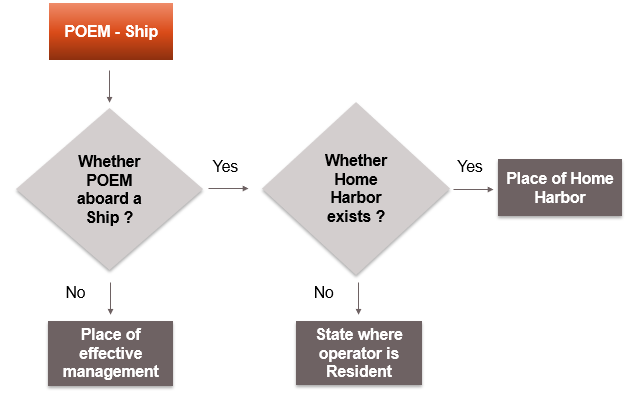

Place of Effective Management – Ship – Article 8(3)

Article 14(4) as per INDIA – Malaysia Treaty

Gains derived by a resident of a Contracting State

from the alienation of shares deriving more than 50% of their value

“directly or indirectly” from immovable property

situated in the Other Contracting state

or

any other right pertaining to such immovable property

may be taxed in that Other State.

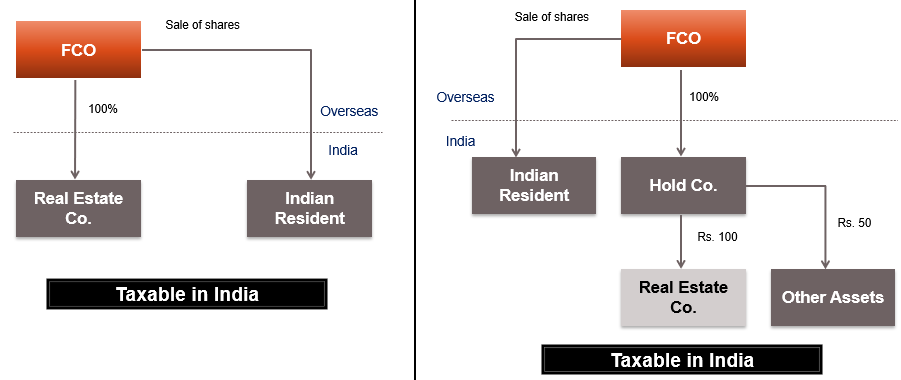

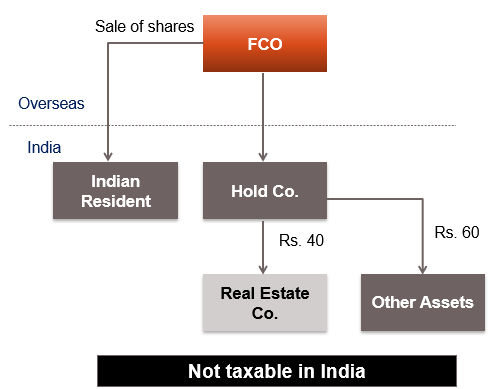

Article 13(4) – Value from Immovable Property

Article 13(4) – Less than 50% Value from IP

Article 13(4)

| Liabilities | Amount (Rs.) | Assets | Amount

(Rs.) |

| Share Capital | 100 | Immovable property | 300 |

| Reserve & Surplus | 200 | Other Assets | 200 |

| Loan for immovable property | 200 | ||

| Total | 500 | Total | 500 |

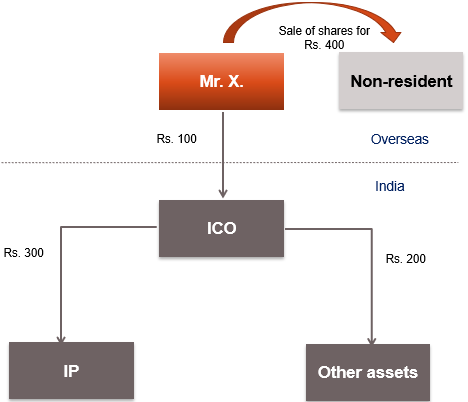

Facts:

- Mr. X owns entire Share capital of Rs. 100 in ICO;

- ICO owns immovable property of Rs. 300 & other assets of Rs. 200;

- ICO has taken loan for immovable property of Rs. 200;

- Mr. X sells shares of ICO to a NR for Rs. 400, and derives Capital Gain of Rs. 300.

Issue:

- Whether Capital Gain will be taxable in India ?

Learn More about “Article 13 – Capital Gains Tax” – Subscribe International Tax Course

Certain Possible Exceptions

- Transfer of shares of Listed companies owning immovable property

- Transfer of shares as a part of corporate reorganizations

- Where business is carried on in the property

- Pension funds, REIT cases

Article 13(5) – India – Netherlands Treaty – Alienation of any other property

Gains from the

alienation of

any property other than that referred to in paragraphs 1, 2, 3 & 4

shall be taxable

only in the State of which the alienator is a resident.

Assets whose transfer could be covered under Residuary Clause

- Shares of an Indian company – Other than Real Estate company covered earlier

- Bonds, Debentures (Convertible/ Non convertible)

- Options and Futures (Stock or Index)

- Movable property not forming part of business

- Trademark & Technology

- Forward cover contracts

- Other financial instruments

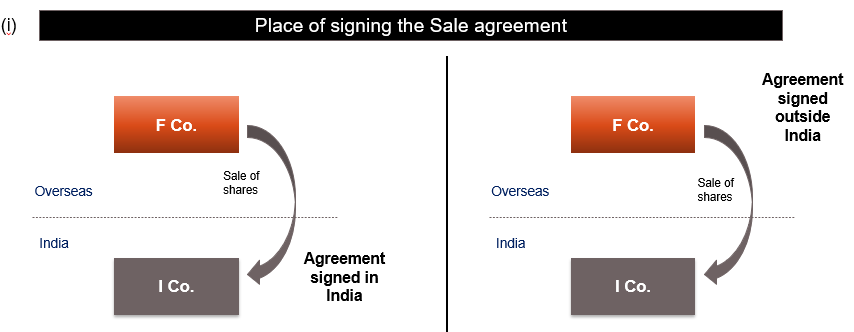

Factors not considered to be relevant while applying Article 13(5)

Learn More about “Article 13 – Capital Gains Tax” – Subscribe International Tax Course

COMPUTATION OF INCOME IN SOURCE STATE

- Article 13 does not provide methodology of computing income in Source State

- Taxable income should be computed as per Domestic law of Source State – Nature and extent of any deductions for expenses, exemption etc to be governed by provision of IT Act

- Proviso 2 to Section 48 – Indexation not available for long term capital asset being shares or Debentures in an Indian company

Capital gains Tax on Transfer of Ship ?

Learn More about “Article 13 – Capital Gains Tax” – Subscribe International Tax Course