Natural resources, covers resources like oil, natural gas, water and deposits of sand and rocks. Under the UAE Constitution, the right to extract such natural resources is with the particular Emirate, where the resource is found. In view of this, Corporate Tax on Natural resources in UAE will not be applicable on the following income : –

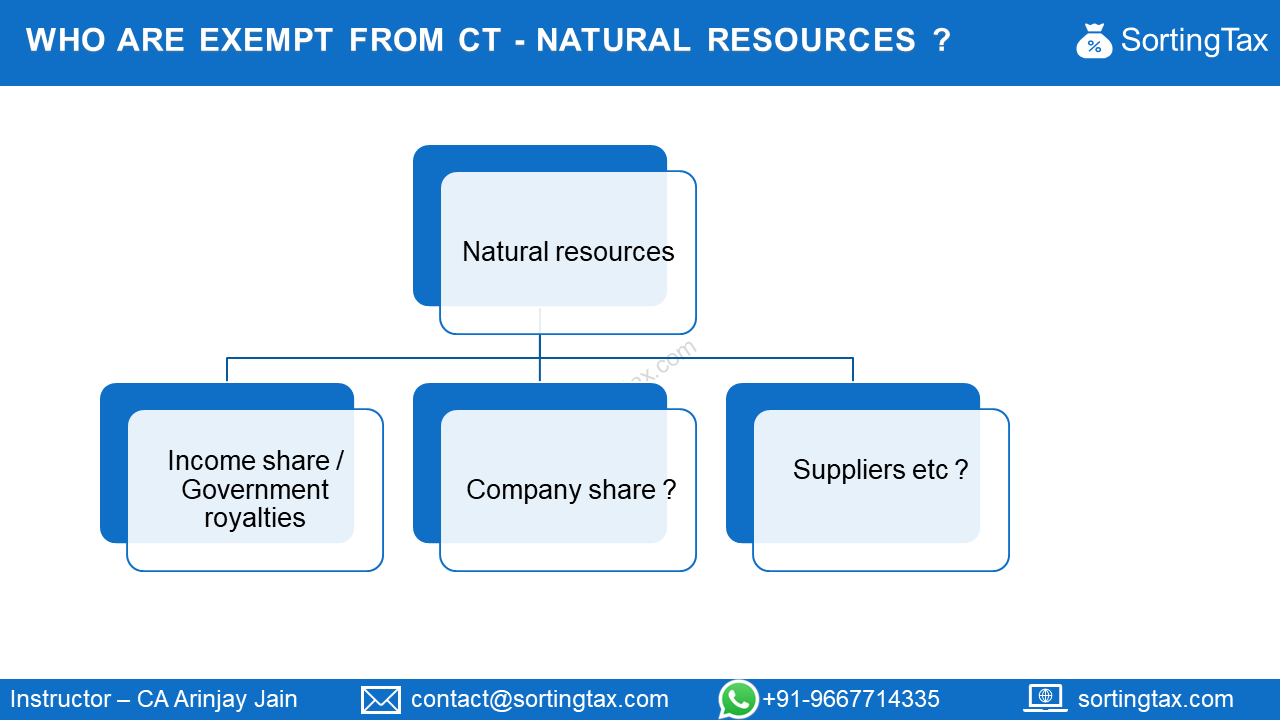

- any income from the extraction and exploitation of natural resources directly earned by the Government

- any share of income from the extraction and exploitation of natural resources directly earned by the Government

- Royalties and other fiscal levies raised by the Government from the extraction or production of natural resources by private sector companies

The extraction of natural resources in Emirate is carried out by various privately owned companies (partly or completely) under long-term concession contracts . Since the extraction of natural resources is not a short-term process , there are long-term contracts which involves long-term commitment , and are entered into between the Emirates and the companies. In case of such contracts, there may be certain taxation which would be applicable at the Emirate level. In view of this, to avoid double taxation, the proposed corporate tax Regime provides that Corporate Tax on Natural resources in UAE , will not apply to such income, provided that the profits earned by such companies are subject to Emirate-level taxation.

Further, the share of the company which is engaged in the extraction and exploitation of natural resource will also be outside the scope of the corporate tax , as such taxation will be governed by the contract entered into by such company with the Emirates . However, income of the suppliers, contractor or other person supporting such company will not be exempt from corporate tax . They will be liable to the corporate taxation.

Learn More about “Corporate Tax on Natural resources in UAE” – Subscribe UAE Corporate Tax Course

Learn More about “Corporate Tax on Natural resources in UAE” – Subscribe UAE Corporate Tax Course