Double Taxation and Connecting Factors – Jurisdictional Double Taxation, Economic Double Taxation and Tax Neutrality – Capital Export Neutrality, Capital Import Neutrality, Nationality Neutrality

Taxability of a foreign entity /taxpayer, in any country depends upon the : –

a) Residence of Taxpayer – Generally, resident are taxable on their global income, while the non resident maybe only taxable on certain income.

b) Source of Income –Generally, income from sources within a country is taxable in that country, while income from sources outside the country is not taxable (unless the income is text based on the residential status).

Doing business with another country

If a foreign entity/taxpayer, is doing business with another country i.e. (source country), it would generally be subject to tax in its home country, based on its residence.

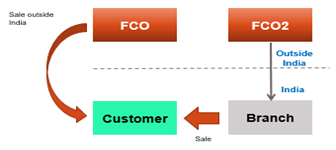

For example, if a foreign company sells certain goods to an Indian customer , where the property in goods is transferred outside India, such transaction would amount to doing business with a country

Doing business in another country

If a foreign entity/taxpayer, is doing business in the host/source country, it will also be taxed in the host country on the basis of its source.

For example, if a foreign company opens a branch office in India and sells certain goods to an Indian customer , such transaction would amount to doing business with a country

DOUBLE TAXATION AND CONNECTING FACTORS – JURISDICTIONAL DOUBLE TAXATION

Jurisdictional double taxation, takes place, when tax is imposed by two or more countries, as per their domestic laws, in respect of the same transaction, on the ground that income arises in their respective jurisdictions.The tax is levied on the same person twice, first in the source country and Secondly in the country of residence.

EXAMPLE ON JURISDICTIONAL DOUBLE TAXATION : –

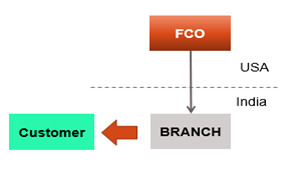

Company FCO is a resident of Country A, and has a branch in India which sells goods to Indian customer. In this example, Country A would be the country of residence for FCO, whereas India would be the country of source since it derives income from sale of goods in India.

India would tax the profits earned by the branch of FCO located in India (as it would constitute a PE of FCO). FCO may also be taxed in Country A, where Country Alevies tax on worldwide income of its residents, including profits of its India branch.

DOUBLE TAXATION AND CONNECTING FACTORS – ECONOMIC DOUBLE TAXATION

Economic double taxation arises when a particular income or capital, is taxed in two or more countries, in the hands of different person. The tax is levied on two different person , even though the transaction is the same.

EXAMPLE: –

In case of Dividend distributed by an Indian company, the Indian company is liable to pay Dividend Distribution Tax. However, the same dividend may be liable for taxation in the country of residence in the hands of shareholders, where no credit may be available for the Dividend Distribution Tax paid in India.

TAX EQUITY

The concept of Tax Equity has two principle elements : –

Fair share of Tax Revenue

If a transaction involve residents of more than one country, each country, whose residents are arty to the contract, must be entitled to its fair share of tax revenue on such income.

No discrimination between residents and non-residents while levying of taxes

If there are any non-resident taxpayers, who are involved in the cross border transactions with a particular country, they should not be subjected to any additional tax , which results in discrimination between residents and non-residents .

Further, the non-residents taxpayers should not be given any undue preference, which is not available to other taxpayers . Generally, these provisions are incorporated in Article 24, relating to Non-Discrimination in the tax Treaties.

TAX NEUTRALITY

Tax Neutrality concept provides, that the tax should be levied in such a manner, that it does not impact the economic processes, i.e, it should not create incentives for taxpayers for the following : –

- To invest more or less in any country due to tax reasons;

- To work more or less in any country due to tax reasons;

- To employ more or less labor in any country due to tax reasons

Tax Neutrality may be of following kind : –

- Capital Export Neutrality

- Capital Import Neutrality

- Nationality Neutrality

Each one of these is discussed as under : –

CAPITAL EXPORT NEUTRALITY

When a person looks at taking an investment decisions on where (which country) to invest, such decision should be based on pure commercial considerations.

The businessman should select a location which fetches maximum pre-tax returns to the business and such decisions should not be affected due to tax factors between country of residence & country of source.

Let us understand this with an illustration

A. Ltd. (Indian resident) – (Amount in Millions)

| Particulars | India

(Tax rate 30%) |

United Kingdom (UK)

(Tax Rate 40%) |

| Sales revenue | 3000 | 3000 |

| Less: Total cost of operations | 1700 | 1500 |

| Profit before tax for the year | 1300 | 1500 |

| Less: Tax Payable | 390 | 600 |

| Net Profit After Tax | 910 | 900 |

In this example, while the pre-tax returns are higher in UK, given that the tax rate in India is lower, the net profit after tax in India is higher than in UK. In such an example, the decision of the businessman to invest in India would be governed by tax reasons, which violates the concept of capital export neutrality.

CAPITAL IMPORT NEUTRALITY

The capital investment in any country can be made by resident of that country (ICO2) or a non resident (FCO).

The Capital Import Neutrality, provides that all investments in a given country, must pay same amount of tax, whether the investment is made by a resident (ICO2) or a non resident (FCO). The tax payable by a non-resident, for the same income in India , should be at the same level, when compared to the tax payable by resident who also derives same income in India.

NATIONAL NEUTRALITY

This concept provides that from a national perspective, foreign income ,earned from sources outside the resident country , must be taxed in the country of residence (FTS income derived by ICO should be taxed in ICO’s country of residence).

However, relief from taxes paid in the foreign country (USA), should be allowed in ICO’s country of residence in the same manner, in which deduction for other costs is allowed to compute taxes. Such a tax system will make investors in ICO’s country of residence , indifferent between the pre-tax return on domestic investments, and the return on foreign investments after paying foreign taxes.

For any queries, please write them in the Comment Section or Talk to our tax expert