Double Taxation Avoidance Agreement – Article 25 Mutual Agreement Procedure

There may be a situation wherein a tax payer may believe that the taxation treatment by the source country is not in accordance with the provisions of tax Treaty. In such a case, he may request his country of resident to initiate mutual agreement procedure to arrive at a consensus with the source country on the interpretation of the tax Treaty.

MUTUAL AGREEMENT PROCEDURE – DEFINITION

MAP is a special facilitative procedure

set out in various tax treaties

that allows designated government representatives of Treaty partners (”referred to as Competent Authorities”)

to work together, and resolve

international tax disputes, including cases of double taxation

arising out of application of the Convention.

APPLICABILITY OF MAP TO VARIOUS ARTICLE

All Articles of the Convention, including specifically

- Business Profits and PE – Article 7 & 5

- Associated Enterprises – Article 9

- Dividends – Article 10

- Interest – Article 11

- Royalties and Fee for technical Services – Article 12

- Elimination of Double taxation – Article 23

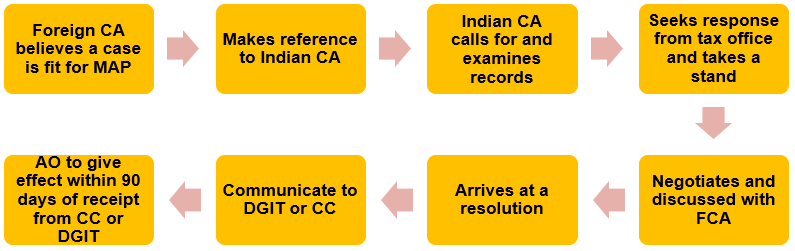

Implementation of MAP is vested with Competent authorities of Treaty countries.

IMPLEMENTATION OF MAP UNDER INDIAN DOMESTIC LAWS

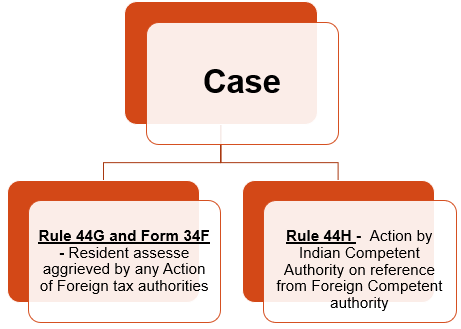

RULE 44G – APPLICATION FOR GIVING EFFECT TO THE TERMS OF ANY AGREEMENT

- Aggrieved resident assesse, for an action of tax authorities of foreign country

- Taxation is bonafide believed to be not in accordance with terms of Treaty

- File application in Form No 34 F to Indian Competent Authority to invoke MAP.

RULE 44H – ACTION BY INDIAN COMPETENT AUTHORITY ON REFERENCE FROM FOREIGN COMPETENT AUTHORITY

If assesse accepts MAP resolution between two CA’s and withdraws relevant pending appeals, AO shall give effect to MAP resolution.

ARTICLE 27(1) OF INDIA US TREATY

Where a person considers

that the actions of one or both of the Contracting States

result or will result for him in taxation not in accordance with the provisions of this Convention,

he may,

irrespective of the remedies provided by the domestic law of those States,

present his case to the competent authority of the Contracting State of which he is a resident or national.

This case must be presented within three years of the date of receipt of notice of the action which gives rise to taxation not in accordance with the Convention.

ARTICLE 25(1) – KEY CHARACTERISTICS

What is covered under “Person” ?

Reference may be made to Article 3 / IT Act (if not defined)

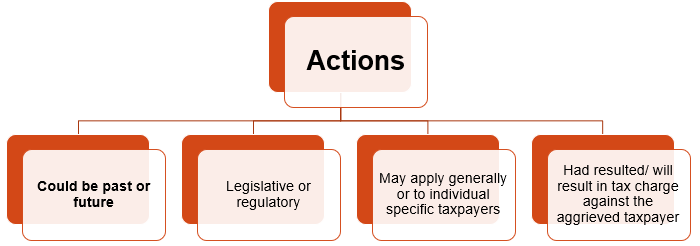

Whose Action can result in MAP ?

Actions of one or both of the Contracting States

What Action are covered ?

Past and Future

What is the belief of the taxpayer ?

Taxation is not in accordance with the provisions of Treaty.

ACTIONS OF CONTRACTING STATE

Actions should give rise to double taxation of same income, which is contrary to the provisions of the Convention.

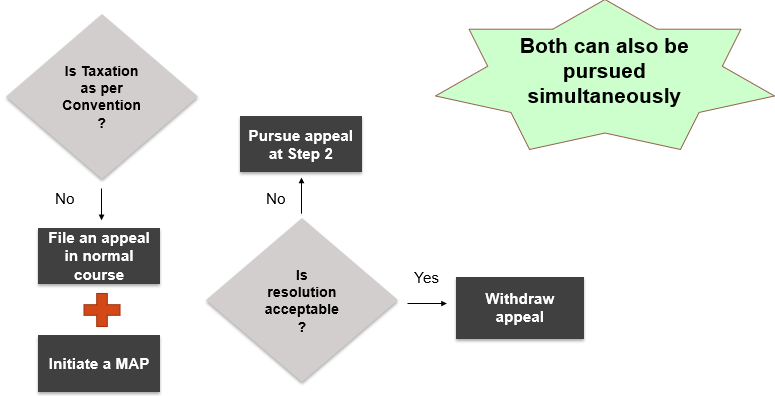

IF TAXATION NOT AS PER CONVETION, REMEDIES TO TAXPAYER IN INDIA

ARTICLE 27(2) OF INDIA US TREATY

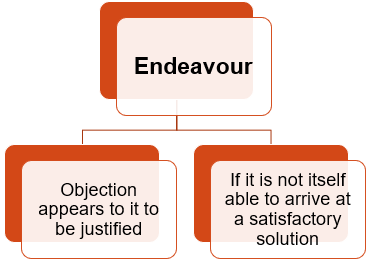

The competent authority shall endeavour,

if the objection appears to it to be justified and if it is not itself able to arrive at a satisfactory solution,

to resolve the case by mutual agreement with the competent authority of the other Contracting State,

with a view to the avoidance of

taxation which is not in accordance with the Convention.

Any agreement reached shall be implemented notwithstanding any time limits or other procedural limitations in the domestic law of the Contracting States.

WHEN SHALL COMPETENT AUTHORITY ENDEAVOUR

FCA may endeavour to resolve case by mutual agreement with an objective of avoiding taxation which is not in accordance with Treaty

ARTICLE 27(3) OF INDIA US TREATY

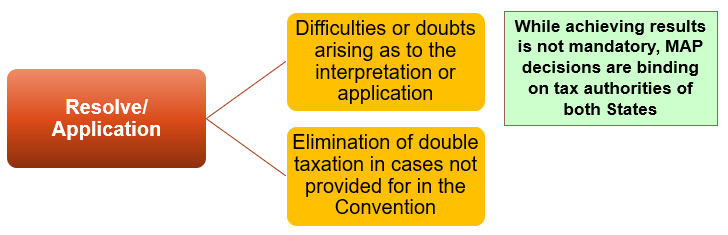

The competent authorities of the Contracting States shall endeavour

to resolve by mutual agreement

any difficulties or doubts arising as to the interpretation or application of the Convention.

They may also consult together for the elimination of double taxation in cases not provided for in the Convention.

SCOPE OF ARTICLE 27(3)

ARTICLE 27(4) OF INDIA US TREATY

The competent authorities of the Contracting States

may communicate with each other directly for the purpose of reaching an agreement in the sense of the preceding paragraphs.

The competent authorities, through consultations,

shall develop appropriate bilateral procedures, conditions, methods and techniques for the implementation of the mutual agreement procedure provided for in this Article.

In addition, a competent authority may devise appropriate unilateral procedures, conditions, methods and techniques to facilitate the above-mentioned bilateral actions and the implementation of the mutual agreement procedure.

BILATERAL PROCEDURES – PAYMENT OF DISPUTED TAX DEMAND PENDING MAP FINALISATION

MoUs with UK, US and Denmark deal with disputed tax collection

INDIA – USA TREATY – MOU FOR STAY OF DEMAND – APPLICABILITY

FACTS CONSIDERED BY AO BEFORE GRANT OF STAY

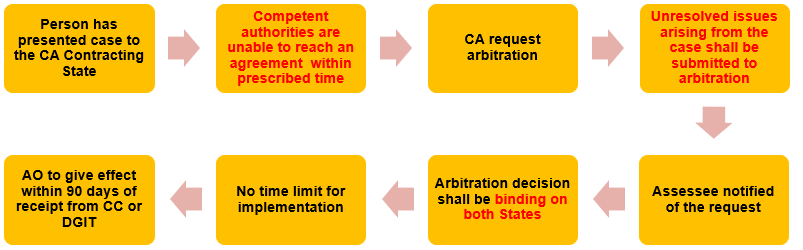

ARBITRATION CLAUSE IN TREATY

Some Treaties give flexibility to CA’s to arrive at alternate solution within specified time

KEY ISSUES / CHALLENGES

- Court decision before MAP is resolved ?

- Court decision after MAP is resolved ?

- No time limit for concluding MAP

- Duty to resolve MAP cases on Individual case merits Vs group resolution

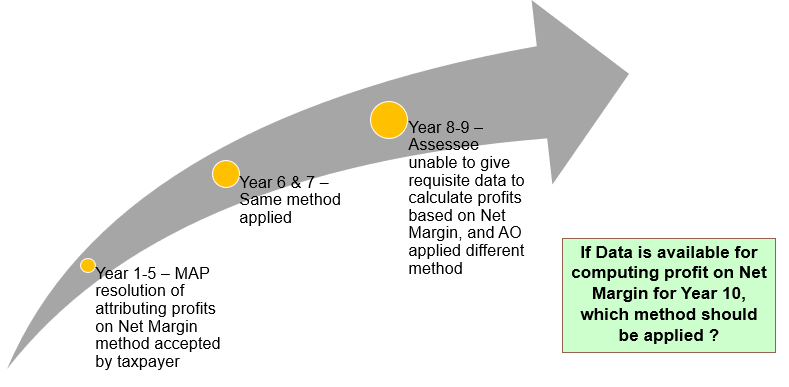

APPLICATION OF MAP FOR SUBSEQUENT YEARS

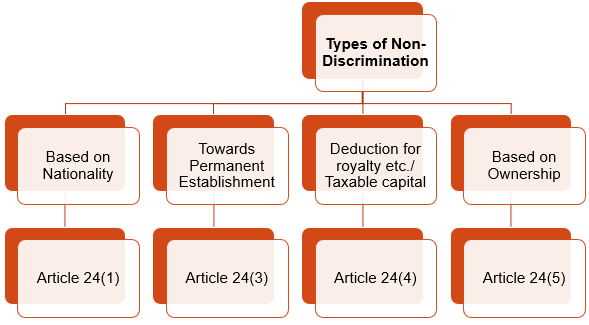

ARTICLE 24 – NON DISCRIMINATION

WHAT IS NON DISCRIMINATION?

Differences in tax treatment of two taxpayers

who are placed in identical/comparable situations

which result in Double taxation for the taxpayer

is Discrimination for tax purpose.

However, where the Treaty itself provides for different treatment

it is not covered under Article 24.

TYPES OF NON – DISCRIMINATION COVERED

ARTICLE 26 (1) – INDIA USA TREATY NON-DISCRIMINATION BASED ON NATIONALITY

Nationals of a Contracting State

shall not be subjected in the other Contracting State

to any taxation or any requirement connected therewith

which is other or more burdensome

than the taxation and connected requirements to which nationals that other State

in the same circumstances are or may be subjected.

This provision shall apply to persons who are not residents of one or both of the

Contracting States.

ARTICLE 24(1) – KEY CHARACTERISTICS

Who are covered?

Nationals of a Contracting State (Stateless person)

What is the ground of discrimination ?

Taxation or any requirement connected therewith

Taxation or any requirement should not be ?

Other or more burdensome than what is applicable to nationals that other State in the same circumstances

Does it apply to NR of both States ?

Yes

Who are Nationals ?

- Individual – Having nationality of a Treaty Partners

- Others – Deriving nationality under laws in force in a Contracting State.

SAME CIRCUMSTANCES ?

“Are the circumstances same between A, B and C ?

| Person | Tax Resident | National |

| Mr. A | India | German |

| Mr. B | India | India |

| Mr. C | Germany | French |

“Are the entities under same circumstances ?

| Entity 1 | Entity 2 |

| Company | Individual |

| Nationalised Bank | Foreign Bank |

| Domestic Company | Foreign company |

ARTICLE 26 (2) – INDIA USA TREATY DISCRIMINATION FOR PE TAXATION

Except where the provisions of paragraph 3 of Article 7 (Business Profits) apply,

the taxation on a permanent establishment which an enterprise of a Contracting State has in the other

Contracting State

shall not be less favorably levied in that other State than the taxation levied on enterprises of that other State

carrying on the same activities.

This provision shall not be construed as obliging a Contracting State to grant to residents of the other

Contracting State any personal allowances, reliefs and reductions for taxation purposes on account of civil

status or family responsibilities which it grants to its own residents.

ARTICLE 26 (2) – INDIA USA TREATY PE TAXATION

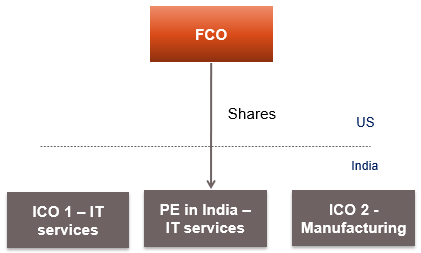

For PE and ICO 1 taxation of PE (business profits) in India shall not be less favorably levied than ICO 1

PE – STAND ON THE FOLLOWING ASPECTS ?

- Deduction of expenses from Royalty and Section 44D restriction ?

- Claim of Tax incentives ?

- Deduction of expenses to compute business profits ?

- WHT on royalty to PE vs a domestic company ?

- Deduction of HO expenses ?

- Applicability of Transfer Pricing provision vis a vis Domestic TP ?

- Carry forward of losses ?

- Group consolidations, tax free transfer of assets between group companies etc ?

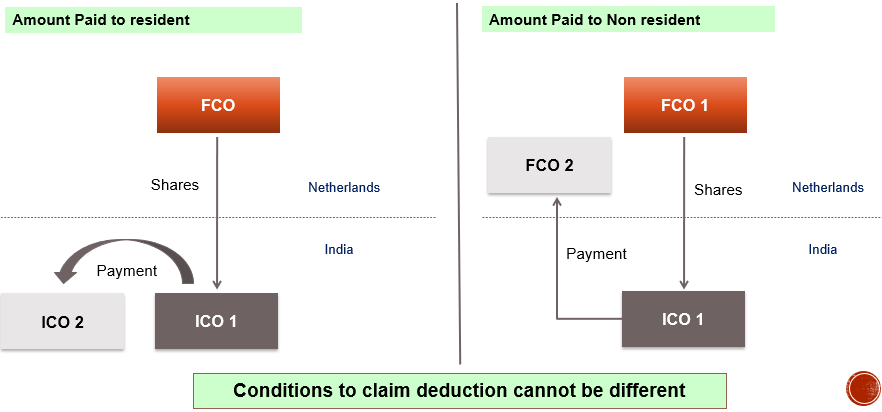

ARTICLE 26 (3) – INDIA USA TREATY NON-DISCRIMINATION DEDUCTION OF EXPENSES

Except where the provisions of paragraph 1 of article 9 (Associated Enterprises), paragraph 7 of article 11 (Interest), or

paragraph 8 of article 12 (Royalties and Fees for Included Services) apply,

interest, royalties, and other disbursements paid by a resident of a Contracting State to a resident of the other Contracting

State shall,

for the purposes of determining the taxable profits of the first-mentioned resident, be deductible under the same

conditions as if they had been paid to a resident of the first-mentioned State.

ARTICLE 26 (3) – INDIA USA TREATY DEDUCTION OF EXPENSES

What is covered?

Interest, royalties, and other disbursements

Whether Paid or accrued ?

Paid

Exceptions

- Paragraph 1 of article 9 (Associated Enterprises),

- Paragraph 7 of article 11 (Interest), or

- Paragraph 8 of article 12 (Royalties and Fees for Included Services) apply

Conditions of deduction

Should be the same

ARTICLE 26 (3) – INDIA USA TREATY DEDUCTION OF EXPENSES

ARTICLE 26 (4) – INDIA USA TREATY OWNERSHIP OF FOREIGN COMPANY

Enterprises of a Contracting State,

the capital of which is wholly or partly owned or controlled, directly or indirectly, by one or more

residents of the other Contracting State,

shall not be subjected in the first-mentioned State to

any taxation or any requirement connected therewith

which is other or more burdensome

than the taxation connected requirements to which other similar enterprises of the first-mentioned State are

or may be subjected.

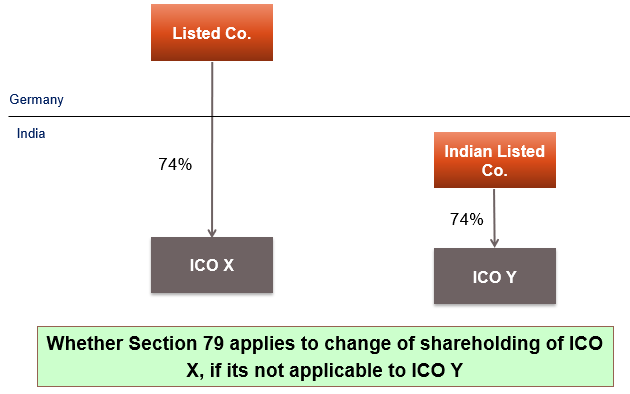

NON APPLICABILITY OF ARTICLE 26(4)

- Transfer pricing Applicability

- Deduction of interest only at the time of payment

- Claim for carry forward of losses due to change in shareholding

INDIA GERMANY TREATY – DAIMLER CHRYSLER CASE

ARTICLE 26 (5) – INDIA USA TREATY

Nothing in this article shall be construed as preventing either Contracting State

from imposing the taxes described in Article 14 (Permanent Establishment Tax) or

the limitations described in paragraph 3 of Article 7 (Business profits).

NON DISCRIMINATION – SPECIFIC EXAMPLES

| Issue | Treaty |

| Chapter VI deduction/ Transfer Pricing provision, based on residential status | Since they are not based on nationality, they are not covered for purpose of Article 24(1) |

| Benefit of indexation on sale of shares and debentures of Indian company | Not allowed to non-residents, and does not amount to discrimination |

| Charge of higher tax rate on a Foreign Company is not a less favorable | Explanation to section 90 |

Learn More about “Double Taxation Avoidance Agreement (DTAA)”