SAFE HARBOUR RULES FOR SPECIFIED DOMESTIC TRANSACTION

CBDT vide Notification No. 11/2015 dated 04.02.2015 in exercise of the powers conferred by section 92CB and 92D, read with section 295, inserted Rules 10TH, 10THA, 10THB, 10THC, & 10THD and has prescribed the safe harbour rules for specified domestic transaction as well.

ELIGIBLE ASSESSEE WHO CAN OPT FOR SAFE HARBOUR RULES – RULE 10THA

Eligible assessee means a person who has exercised a valid option for application of safe harbour rules, and who is a : –

- Government company engaged in the business of generation, supply, transmission or distribution of electricity; or

- co-operative society engaged in the business of procuring and marketing milk and milk products.

DEFINITION OF GOVERNMENT COMPANY AS PER SECTION 2(45) OF THE COMPANIES ACT, 2013:

Government company means any company

in which 51% or more

of the paid-up share capital

is held by State Government or Governments, or

partly by the Central Government and partly by one or more State Governments, and

includes a company which is a subsidiary company of such a Government company.

ELIGIBLE SPECIFIED DOMESTIC TRANSACTION FOR SAFE HARBOUR RULES – RULE 10THB

THE ELIGIBLE SPECIFIED DOMESTIC TRANSACTION MEANS A SPECIFIED DOMESTIC TRANSACTION UNDERTAKEN BY AN ELIGIBLE ASSESSEE AND WHICH COMPRISES OF : –

- supply of electricity; or

- transmission of electricity ; or

- wheeling of electricity; or

- purchase of milk or milk products by a co-operative society from its members.

SAFE HARBOUR – CIRCUMSTANCES (RULE 10THC)

The transfer price declared by the eligible assessee in respect of specified domestic transactions shall be accepted by the income-tax authorities, if it is in accordance with followings circumstances:

| Eligible Specified Domestic Transaction | Circumstances |

|

The tariff in respect of supply or transmission or wheeling of electricity is determined by Appropriate Commission or the methodology for determination of the tariff is approved by Central Regulatory Commission referred to in Section 76 (1) or the State Regulatory Commission referred to in Section 82 or the Joint Commission referred to in section 83 of the Electricity Act, 2003. |

|

The price of milk or milk products is determined at a rate which is fixed on the basis of the quality of milk, namely, fat content and Solid Not FAT (SNF) content of milk and –

a) the said rate is irrespective of,- i. the quantity of milk procured; b) such prices are routinely declared by the co-operative society in a transparent manner and are available in public domain |

The transfer price declared by the eligible assessee in respect of specified domestic transactions shall be accepted by the income-tax authorities, if it is in accordance with followings circumstances:

NO COMPARABILITY ADJUSTMENT AND ALLOWANCE : –

No comparability adjustment and allowance under the second proviso to section 92C(2) (i.e. Arithmetic Mean or Range concept) shall be made to the transfer price declared by the assessee and accepted by the income-tax authority.

MAINTENANCE OF INFORMATION AND DOCUMENTS : –

The provisions relating to maintenance of information and document and submission of report in Form No. 3CEB in respect of specified domestic transaction shall apply irrespective of the fact that the assessee exercises his option for Safe Harbour Rules.

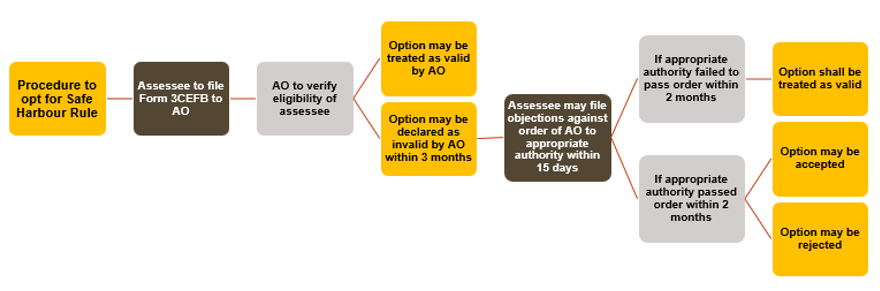

PROCEDURE UNDER SAFE HARBOUR RULES FOR SPECIFIED DOMESTIC TRANSACTION – RULE 10THD

I. FURNISHING OF FORM 3CEFB : –

a) The assessee shall furnish a Form 3CEFB to the Assessing Officer on or before due date of furnishing of return of income for exercising the option of safe harbour.

II. VERIFICATION BY ASSESSING OFFICER : –

On receipt of Form 3CEFB the assessing officer shall verify whether

- The assessee exercising the option is an eligible assessee; and

- The transaction in respect of which option is exercised is an eligible specified domestic transaction

before the option for safe harbour by the assessee is treated to be validly exercised.

III. NOTICE FOR FURNISHING OF INFORMATION OR DOCUMENTS : –

Where the Assessing Officer doubts the valid exercise of safe harbour option he may require the assessee, to furnishing information or documents or other evidence as he may consider necessary, within the time specified in such notice.

IV. ORDER DECLARING SAFE HARBOUR OPTION AS INVALID : –

Where –

- the assessee does not furnish the information or documents or other evidence required by the Assessing Officer; or

- the Assessing Officer finds that the assessee is not an eligible assessee; or

- the Assessing Officer finds that the specified domestic transaction in respect of which the safe harbour option has been exercised is not an eligible specified domestic transaction; or

- the tariff is not in accordance with the circumstances specified for eligible specified domestic transaction,

the Assessing Officer shall, by order in writing, declare the option exercised by the assessee to be invalid and cause a copy of the said order to be served on the assessee:

However no order declaring the option exercised by the assessee to be invalid shall be passed without giving an opportunity of being heard to the assessee.

V. TIME LIMIT FOR DECLARING SAFE HARBOUR OPTION AS INVALID BY ASSESSING OFFICER : –

The Assessing Officer shall pass the order declaring the option exercised by the assessee as invalid within a period of 3 months from the end of the month in which Form 3CEFB is received by him.

No order can be passed by Assessing Officer declaring the option as invalid unless an opportunity of being heard is given to the assessee.

VI. FILING OF OBJECTIONS AGAINST THE ORDER OF ASSESSING OFFICER DECLARING THE OPTION TO BE INVALID : –

If the assessee objects to the order of the Assessing Officer declaring the option to be invalid, he may file his objections with the Principal Commissioner or the Commissioner or the Principal Director or the Director, to whom the Assessing Officer is subordinate, within 15 days of receipt of the order of the Assessing Officer.

VII. RECEIPT OF OBJECTION AGAINST THE ORDER OF ASSESSING OFFICER DECLARING THE OPTION TO BE INVALID : –

On receipt of the objection from assessee the Principal Commissioner or the Commissioner or the Principal Director or the Director, shall pass appropriate order, within a period of 2 months from the end of the month in which the objection filed by the assessee is received, after providing an opportunity of being heard to the assessee.

VIII. DEEMED ACCEPTANCE OF SAFE HARBOUR OPTION : –

If the Assessing Officer or the Principal Commissioner or the Commissioner or the Principal Director or the Director, does not pass an order within aforesaid time then the option for safe harbour exercised by the assessee shall be treated as valid.

INFORMATION AND DOCUMENTS TO BE KEPT AND MAINTAINED FOR SPECIFIED DOMESTIC TRANSACTION – RULE 10D(2A)

INFORMATION AND DOCUMENTS TO BE KEPT AND MAINTAINED BY GOVERNMENT COMPANY ENGAGED IN THE BUSINESS OF GENERATION, SUPPLY, TRANSMISSION, OR DISTRIBUTION OF ELECTRICITY ARE AS FOLLOWS : –

- a description of the ownership structure of the assessee enterprise with details of shares or other ownership interest held therein by other enterprises;

- a broad description of the business of the assessee and the industry in which the assessee operates, and of the business of the associated enterprises with whom the assessee has transacted;

- the nature and terms (including prices) of specified domestic transactions entered into with each associated enterprise and the quantum and value of each such transaction or class of such transaction;

- a record of proceedings, if any, before the regulatory commission and orders of such commission relating to the specified domestic transaction

- a record of the actual working carried out for determining the transfer price of the specified domestic transaction;

- the assumptions, policies and price negotiations, if any, which have critically affected the determination of the transfer price; and

- any other information, data or document, including information or data relating to the associated enterprise, which may be relevant for determination of the transfer price;

INFORMATION AND DOCUMENTS TO BE KEPT AND MAINTAINED BY A CO-OPERATIVE SOCIETY ENGAGED IN THE BUSINESS OF PROCURING AND MARKETING MILK AND MILK PRODUCTS : –

- a description of the ownership structure of the assessee co-operative society with details of shares or other ownership interest held therein by the members;

- description of members including their addresses and period of membership;

- the nature and terms (including prices) of specified domestic transactions entered into with each member and the quantum and value of each such transaction or class of such transaction;

- a record of the actual working carried out for determining the transfer price of the specified domestic transaction;

- the assumptions, policies and price negotiations, if any, which have critically affected the determination of the transfer price;

- the documentation regarding price being routinely declared in transparent manner and being available in public domain; and

- any other information, data or document which may be relevant for determination of the transfer price.

For any queries, please write them in the Comment Section or Talk to our tax expert