Bird’s Eye view of the ‘Deemed interest income’

| Concept of taxation | Non-Resident Taxation |

| Provision of Income Tax Act, 1961 | Section 9(1)(v) |

| Provision deals with | Interest payable deemed to accrue or arise in India |

Deemed Interest Income – Section 9(1)(v) of Income Tax Act

Interest payable to the non- resident , could be from the following Payors : –

- Interest payable by Indian Government

- Interest payable by a Indian resident to non-resident

- Interest payable by one non-resident to another non-resident

The circumstances under which such interest is deemed to accrue or arise in India are discussed as under : –

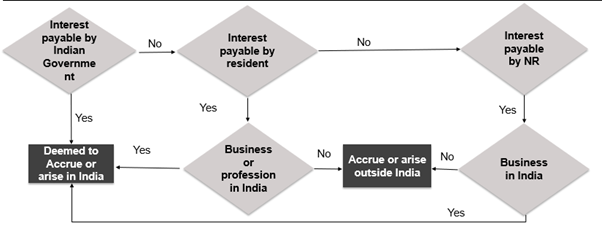

Interest Payable by Indian Government Deemed to Accrue or Arise in India – Section 9(1)(v)

Under section 9(1)(v) of Income Tax Act, interest payable by the Indian Government (whether Central Government or the State Government) to any non-resident, shall be deemed to accrue or arise in India.

NOTE : –

Such Interest shall always be deemed to accrue or arise in India without any exceptions.

Interest Payable by a Resident Deemed to Accrue or Arise in India – Section 9(1)(v) of Income Tax Update

Under section 9(1)(v), interest payable by any person who is a resident in India, to a non-resident , shall be deemed to accrue or arise in India , unless it falls under the following two exceptions : –

- Interest is payable for money borrowed and used for the purposes of a business or profession carried on by person outside India ; or

- Interest is payable for earning any income from any source outside India.

However, one should note, that where money has been borrowed for any of the two above purposes, but is actually used in a business or profession in India or earning income in India, it shall be deemed to accrue or arise in India in the hands of the non-resident.

Interest Payable by Non-Resident Deemed to Accrue or Arise in India – Section 9(1)(v)

Interest payable by one non-resident to another non-resident, shall be deemed to accrue or arise in India if such interest is payable, in respect of any debt incurred or moneys borrowed and used for the purpose of a business or profession carried on by such non-resident in India.

NOTE : –

Interest on money borrowed by the non-resident for any purpose other than a business or profession, will not be deemed to accrue or arise in India.

Summary of income by way of interest which shall be deemed to accrue or arise in India – Section 9(1)(v) of Income Tax Act

Flow Chart to decide whether interest to Non-Resident is liable to tax in India

Example 1

XYZ India has entered into an agreement with a Mauritius company for importing raw material. In order to make payment for such imports, it avails buyer’s credit from ABC bank, located in Mauritius. Whether interest payment made by ICO to ABC bank under buyer’s credit would be considered as, income which deemed to accrue or arise in India?

Solution

Interest payment made by a person who is a resident in India, would be deemed to accrue or arise in India, where money is borrowed for the purpose of business or profession carried on by such resident in India.In this case interest on buyer’s credit , is paid by ICO for the purpose of its business in India. Thus, such interest income would be deemed to accrue or arise in India.

Example 2

Non-resident ‘X’ , engaged in manufacture of computer software, borrows money from another non-resident ‘Y’, and invests the same in shares of an Indian company for investment purposes.Whether interest payable by ‘X’ to ‘Y’ would be deemed to accrue or arise in India?

Solution

Interest on money borrowed by a non-resident, for any purpose other than a business or profession, will not be deemed to accrue or arise in India. In this case money was borrowed for the purpose of investment and not for the purpose of business or profession of non-resident X. Thus, interest payable by X would be deemed to accrue or arise outside India.

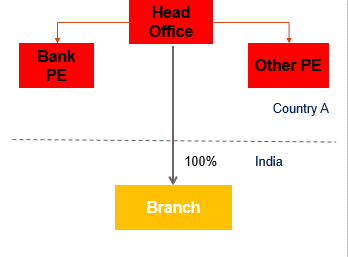

Taxability of Interest Payable by the Indian PE of Foreign Bank – Explanation to Section 9(1)(V) of Income Tax Act

In many cases, a foreign bank which intends to do business in India, instead of opening a company, main open a branch in India. Such a branch is considered as a Permanent Establishment of the foreign bank in India. If such branch makes interest payment to the head office, the issue which arises is, whether such payment are liable to tax in the hands of the head office ?

Prior to the amendment carried out by Finance Act 2015 , while the interest payment were considered as a deductible expenditure in the hands of the Indian branch, such receipts were considered as non taxable in the hands of the head office, on the ground that these payment , constituted as payment to self which were not liable to taxation.

Finance Act 2015, made certain amendments, whereby interest payable by Indian PE of foreign bank, would be deemed to accrue or arise in India if recipient is : –

- Head office of bank located outside India ; or

- PE of bank located outside India; or

- Any other branch outside India.

Points to Consider :-

- Indian PE is obliged to deduct tax at source on any interest payable to either the head office or any other branch or pe, etc. Of the non-resident bank outside india.

- Non-deduction would result in disallowance of interest expenditure and may also attract levy of interest and penalty.

Example 1

Silsila Bank , is located in Mauritius and has a branch in India. In order to meet the funding requirements, the Indian Branch, borrows money from head office in Mauritius on which an interest is charged at LIBOR + 200 basis points? Outline the tax treatment of interest payment made by Indian Branch to Mauritius Head Office ? What would be the tax rate if Article 11(1) and Article 11(2) of the India Mauritius Treaty reads as under : –

- Interest arising in a Contracting State and paid to a resident of the other Contracting State may be taxed in that other State.

- However, such interest may also be taxed in the Contracting State in which it arises, and according to the laws of that State, but if the beneficial owner of the interest is a resident of the other Contracting State, the tax so charged shall not exceed 7.5 per cent of the gross amount of the interest;

You may assume that the Tax rate is 20% under the IT Act, and Silsila Bank is beneficial owner of such interest and eligible for benefit of India Mauritius Treaty ?

Solution

Interest paid by Indian Branch , which constitutes a PE of the Mauritius Head Office, would be deemed to accrue or arise in India, as per Explanation to Section 9(1)(v) of Income Tax Act and would be taxable in India, subject to Treaty benefits.

The Indian PE would be liable to withhold tax on such interest, unless the Treaty provides for exemption of taxation of such interest in India.

According to Article 11 (1) , since interest arises in India, India has a right to tax such interest. Given that Silsila Bank is beneficial owner of such interest and is also eligible for benefit of India Mauritius Treaty , it can opt to be governed by lower tax rate of 7.5 percent provided in the Treaty against 20% under the IT Act .

For any queries, please write them in the Comment Section or Talk to our tax expert