Bird’s Eye view of the ‘Taxation of offshore funds in India’

| Concept of taxation | Non-Resident Taxation |

| Provision of Income Tax Act, 1961 | Section 9A |

| Provision deals with | Taxation of offshore funds in India |

Section 9A Tax on Offshore Funds India is important for overseas mutual funds that invest in Indian equities, debt and other instruments. But in order to understand about this, one should first understand What are Offshore funds?

Offshore funds are mutual fund schemes, which invest in equities of a region or country, or fixed income securities in international markets . Offshore funds can be country-specific (US, India, Brazil), region-specific and thematic funds (funds which invest in sectors such as consumption, energy and real estate etc) .

Generally, an offshore fund has a manager (normally called the fund manager) and a board, which decides where the funds have to be invested, how much funds have to be invested and other decisions related to the funds. The tax issue which normally comes is, where is the place of effective management of such funds and consequently where does the liability to pay tax arise in respect of the income of such funds ?

Generally, such funds are located in tax havens or countries where the tax rate is very low or there are favorable tax treaties with the jurisdiction where the investments are proposed to be made.

Since the management of such funds is predominantly done by the fund manager, generally the place of effective management is considered to be situated in the jurisdiction where the fund manager is located.

Basis of Tax on Offshore Funds India under Section 9A

Section 9(1)(i) provides circumstances, under which income is deemed to accrue or arise in India, and is accordingly, taxable in India. One of the conditions for the income of a non-resident to be deemed to accrue or arise in India is the existence of a business connection in India. Once such a business connection is established, income attributable to the activities which result in a business connection is taxable in India.

Similarly, under Double Taxation Avoidance Agreements (DTAAs), the source country (for example India) assumes taxation rights on certain incomes if the non-resident has a Permanent Establishment (PE) in that country (India).

An offshore fund , may have the presence of a fund manager in India, which may constitute business under normal circumstances, given the broad definition. In view of this, to ascertain whether an offshore fund is liable to tax in India, we need to evaluate whether the presence of the fund manager in India, can either constitute a business connection or a permanent establishment of the offshore fund in India.

The provisions relating to taxation of Offshore funds in India, can be broadly divided into two time frames : –

- Provisions prior to the amendment of section 9A

- Provisions of section 9A

These are discussed as under : –

Taxability of Offshore Funds – Pre amendment provision

Fund manager investing into Indian companies

Under the erstwhile provisions, presence of a fund manager of a non-resident fund in India , carrying out the activity of investing into Indian companies, may constitute a business connection of such fund in India, even though the fund manager may be an independent person. For example, if a Mauritius Fund made investment in Indian company, but the fund Manager was in India, it may have resulted in profits on such investments to be liable to tax in India.

Fund manager investing into overseas companies

Further, fund managers, who were located in India, but undertaking fund management activity of overseas investments for an off-shore fund, may also have caused the profits on such investments to be liable to tax in India. For example, if a Mauritius Fund made investment only in African countries, but the fund Manager was in India, it may have resulted in profits on such investments to be liable to tax in India .

Section 9A Tax on Offshore Funds India – Post Amendment Provision

In order to facilitate the location of fund managers of off-shore funds in India, Section 9A was introduced . It provides as under : –

a) No business connection for offshore funds due to location of fund manager in India – Section 9A(1) : –

The fund management activity carried out through an Eligible Fund Manager (discussed later) acting on behalf of Eligible Investment Funds (discussed later) shall not constitute business connection in India of the said fund.

In other words, the following conditions should be satisfied so that the fund manager does not become the business connection of the Offshore fund in India : –

- The fund manager should be an Eligible Fund Manager ; and

- The fund manager should be acting on behalf of Eligible Investment Funds .

Section 9A tax on offshore funds India – Tax on other income of eligible investment fund

However, Section 9A shall not result in non-taxation of any income of the eligible investment fund, which would have been chargeable to tax, irrespective of whether the activity of the eligible fund manager constituted the business connection in India of such fund or not. For example, if the eligible investment fund owned certain real estate in India, in addition to the investment in the Indian properties, income from such real estate investment would continue to be taxable as per the normal provision.

Section 9A tax on offshore funds India – Tax on other income of eligible fund manager

Further, Section 9A shall not impact the scope of total income or determination of total income of the eligible fund manager himself. This implies that if the eligible fund manager is a tax resident of India/ not a tax resident of India, his/her taxation would not be impacted by the fact about whether the fund is liable to tax in India or not.

b) Offshore funds not to be deemed as resident in India due to location of fund manager in India – Section 9A(2) : –

Where an Offshore fund has investments outside India, and a fund manager in India undertakes Fund management activity in respect of such investments , income of the fund from such investments would not be taxable in India merely because the fund manager located in India. However, if the Offshore fund, is otherwise liable to tax in India, for any other reason (for example, where the Offshore fund is a company which is the resident of India under POEM criterions) , then the income of such Offshore fund may be taxable in India.

A. Meaning of eligible investment fund – Section 9A(3)

Eligible Investment fund means a fund , which is established or incorporated or registered outside India, and collects funds from its members for investing it for their benefit. In addition, such a fund should satisfy the following conditions : –

- The Fund should be a person resident outside India and should not be a person resident in India;

- The Fund should be a : –

- Resident of a country with which India has entered into a DTAA; or

- From AY 2017-18, established/registered or incorporate in a specified territory notified by the Government.

- The aggregate participation or investment in the fund, directly or indirectly, by persons resident in India should not be more than 5%of the corpus of the fund;

- The fund and its activities are subject to applicable investor protection regulations in the country or specified territory where it is established or incorporated or is a resident.

Note : –“CORPUS” MEANS THE TOTAL AMOUNT OF FUNDS RAISED FOR THE PURPOSE OF INVESTMENT BY THE ELIGIBLE INVESTMENT FUND AS ON A PARTICULAR DATE - The fund has a minimum of 25 members who are, directly or indirectly, not connected persons.

- Any member of the fund along with connected persons shall not have any participation interest, directly or indirectly, in the fund above 10%;

- The aggregate participation interest, directly or indirectly, of 10 or less members along with their connected persons in the fund, shall be less than 50%.

Note : –

Conditions at 5, 6 & 7 shall not apply in case of an investment fund set up by the- Government or

- Central Bank of a foreign State or

- A sovereign fund, or

- Such other fund as the Central Government may notify – The Government has notified investment fund set up by Category I or Category II Foreign portfolio investor registered SEBI(Foreign Portfolio Investors) Regulations 2014.

- The fund shall not invest more than 20% of its corpus in any entity;

- The fund shall not make any investment in its associate entity

Associate Means

An entity in which –

a) a director or a trustee or a partner or a member or a fund manager of the investment fund holds, > 15% of its capital or interest either individually or collectively.

or

b) a director or a trustee or a partner or a member of the fund manager of such fund, holds, > 15% of its capital or interest either individually or collectively. - The monthly average of the corpus of an existing fund shall be Rs 100 crore or more. Further, if the fund has been established or incorporated in the previous year, the corpus of fund shall be Rs 100 crore or more at the end of such previous year or within 6 months from the end of the month of its incorporation, whichever is later. This condition shall not be applicable if the fund has been wound up during the year.

- The fund shall not carry on or control and manage, directly or indirectly, any business in India;

- The fund is neither engaged in any activity which constitutes a business connection in India nor has any person acting on its behalf whose activities constitute a business connection in India [other than the activities undertaken by the eligible fund manager on its behalf].

- The remuneration paid by the fund to an Eligible Fund Manager in respect of fund management activity undertaken by him on its behalf should be at Arm’s Length Price of the said activity.

Notes : – [Rule 10V]- The Arm’s Length Price of remuneration paid to fund manager shall be computed as per provisions of transfer pricing.

- The Fund Manager is required to keep and maintain TP documents and he is required also required to furnish TP report in Form 3CEJ in addition to the filing requirements u/s 92E.

B. Meaning of eligible fund manager – Section 9A(4)

The eligible fund manager, in respect of an eligible investment fund, means any person who is engaged in the activity of fund management and fulfils the following conditions :—

- He should not be an employee of the eligible investment fund or an employee of a connected person of eligible investment fund ;

- He should be registered as a fund manager or an investment advisor, in accordance with the SEBI Regulations;

- He should be acting in the ordinary course of his business as a fund manager.

- Eligible investment fund manager, along with his connected persons, shall not be entitled, directly or indirectly, to more than 20% of the profits accruing or arising to the eligible investment fund from the transactions carried out by the fund through the fund manager.

C. Meaning of connected person – Section 9A(9)

“Connected person” means any person who is connected directly or indirectly to another person and includes,

- any relative of the person, if such person is an individual ;

- any director of the company or any relative of such director, if the person is a company ;

- Any partner or member of a firm or association of persons or body of individuals or any relative of such partner or member, if the person is a firm or association of persons or body of individuals ;

- any member of the Hindu undivided family or any relative of such member, if the person is a Hindu undivided family ;

- any individual who has a substantial interest in the business of the person or any relative of such individual ;

- a company, firm or an AOP or a BOI, whether incorporated or not, or a HUF having a substantial interest in the business of the person or any director, partner, or member of the company, firm or AOP or BOI or family, or any relative of such director, partner or member ;

- a company, firm or AOP or BOI, whether incorporated or not, or a HUF, whose director, partner, or member has a substantial interest in the business of the person, or family or any relative of such director, partner or member ;

- any other person who carries on a business, if –

-

- the person being an individual, or any relative of such person, has a substantial interest in the business of that other person ;

- the person being a company, firm, association of persons, body of individuals, whether incorporated or not, or a Hindu undivided family, or any director, partner or member of such company, firm or association of persons or body of individuals or family, or any relative of such director, partner or member, has a substantial interest in the business of that other person.

D. Annual statement by eligible investment fund – Section 9A(5)

Furnishing of annual statement : –

Every eligible investment fund, shall furnish annual statement in Form No. 3CEK to the prescribed income-tax authority, in respect of its activities in a Financial Year.

Due date for furnishing of annual statement: –

Annual statement in Form No. 3CEK shall be furnished within 90 days from the end of the Financial Year.

Electronic filing of annual statement : –

The annual statement in Form No. 3CEK shall be furnished electronically under digital signature

Information to be furnished in annual statement: –

The Form No. 3CEK should contain information relating to : –

- Fulfilment of conditions to qualify as an eligible investment fund; and

- Such other prescribed information or documents.

Penalty on fund

In case of non furnishing of the prescribed statement, information or documents, the fund shall be liable for penalty of Rs. 5,00,000

Example :-

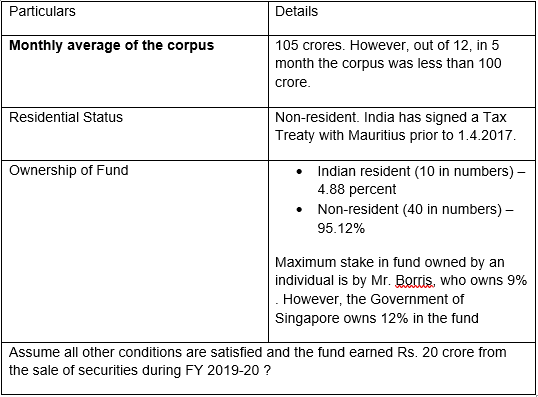

Infinity Partners Mauritius is an investment fund, incorporated on 1.4.2018 and is registered with SEBI. It invests in equity capital of the Indian companies. Based on the following data, you are required to compute the taxable income of the Fund, assuming it is constituted as a Company : –

Solution : –

In the present case, the fund would qualify as an Eligible Fund u/s 9A since it satisfies all the conditions and therefore its income will not be taxable in India : –

For any queries, please write them in the Comment Section or Talk to our tax expert